AFR Article 25 September 2021 page 30

Safety margin Understand how much of your income should be going towards your home loan without pushing you over the edge, writes Duncan Hughes.

Shannon Day-Herbert’s plan to buy a family home on Sydney’s northern beaches has been dashed by rising prices pushing the annual income needed to service a median Sydney house purchase to $197,000.

Day-Herbert, a preschool teacher, and her partner, Peter Matthews, a lawyer, have been outbid by buyers with more cash for a deposit or a bigger appetite for debt.

‘‘We have grown up in this area and wanted to marry and raise our family here,’’ says Day-Herbert, explaining why they wanted to buy in Curl Curl, about 19 kilometres north-east of Sydney’s central business district.

Median house prices in the coastal suburb have jumped more than 30 per cent in the past year to more than $3 million, according to CoreLogic, which monitors property markets.

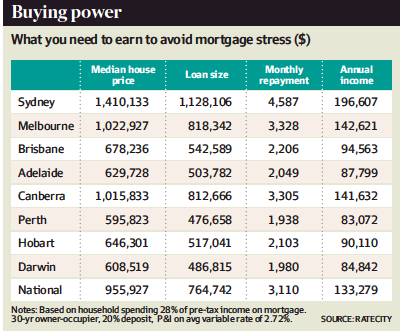

The relentless rise in property prices means that average incomes are no longer enough to afford a house without causing mortgage stress in all state capitals except Perth and Darwin. Mortgage stress is defined as paying more than 30 per cent of household pre-tax income on mortgage repayments.

In Sydney, a person on the average full-time salary of $92,000 with a 20 per cent deposit for a $1.4 million house would need another $105,000 income a year to avoid the stress threshold on one income. (See table, which assumes the buyer has a 30-year principal and interest, owner-occupier loan with a headline variable rate of 2.72 per cent.) These calculations are based on someone paying 28 per cent of their pre-tax income, to allow for increases to mortgage rates without tipping over into mortgage stress.

Day-Herbert and her partner will seek to avoid the stress of a big mortgage by looking for a cheaper house on the Central Coast, further north of Sydney.

For buyers in Melbourne and Canberra, where median house prices are about $1 million, a household would need to have a combined income of more than $140,000 to purchase on the same terms and conditions as the Sydney buyer. Average wages in those cities are $91,000 and $99,000 respectively.

‘‘Price rises for anyone already in the housing market can work in your favour, particularly for investors,’’ says Sally Tindall, research director for RateCity, which compares rates and financial products. ‘‘But owning a house is getting further and further out of reach for those trying to get in.’’

Household debt to income is rising for many households as incomes fall because of COVID-19, even though record low interest rates are keeping a lid on monthly mortgage repayments.

‘‘Buyers might be getting the green light from the banks, but they are still shooting themselves in the foot by taking on high levels of debt,’’ Tindall says.

A combination of rising prices, increased debt and the impact of COVID-19 on income are contributing to mortgage stress beyond the 40 per cent of households on lowest incomes that it traditionally affects, say analysts.

Reduced hours, lower bonuses, unemployment or disrupted household cash flow are pushing mortgage stress to a record high of more than 1.5 million households (equivalent to about 42 per cent of mortgage holders), according to Digital Finance Analytics.

Fiona Guthrie, chief executive of Financial Counselling Australia, says people who have never needed help before are calling its National Debt Helpline seeking financial assistance.

Guthrie says mortgage stress issues are on the rise, particularly in NSW and Victoria, with about one in four small businesses saying they are not continuing or planning to reopen.

‘‘People have less money because they have fewer work hours or have lost their jobs,’’ she says. ‘‘Small businesses are struggling and unable to keep staff on and pay all their loans and bills.’’

Information on mortgage issues has risen to the second most frequently visited section on Financial Counselling Australia’s website, after general information about surviving a financial crisis.SI

10 tips for creating a buffer zone

Try not to overstretch yourself no matter how tempting it might be to take out a bigger loan for the ‘‘dream home’’. Ensure you have a buffer so you can absorb a rate rise of 1 per cent or 2 per cent.

Work your way up the property ladder. If you can’t afford a house in your preferred suburb, consider a unit or another suburb.

Think about relocating out of expensive cities. It’s an increasingly popular way of dealing with rising costs and has been made easier with working from home. Popular locations are typically about two hours’ drive from workplaces, with good roads and rail links.

Look at becoming a ‘‘rentvestor’’. This is where you rent where you want to live but buy an investment property where you can afford.

Consider an offset account that is linked to the home loan and can help reduce interest paid. Any money in the account can be used to offset the balance of the loan, reducing the amount of interest charged each month.

Consider a split loan. It involves having part of the home loan balance charged at a variable rate and part at a fixed rate. Borrowers can choose how to split the loan. It means borrowers have the flexibility of an offset account and can make extra repayments on the variable rate.

Cut back on expenses and debts. Review discretionary spending such as streaming services or gym memberships to see what can be reduced.

Don’t just rely on the bank to tell you how much you can borrow. ‘‘Work out how much you are comfortable with,’’ Tindall says. Most banks provide a loan calculator setting out how much you can comfortably borrow assuming different scenarios, such as starting a family.

Pay down as much as you can while rates are low.

Regularly shop around for a cheaper mortgage. Lenders are competing for new business and will offer better rates for borrowers with a good repayment history who have built up equity in their property. There are plenty of mortgages with headline rates below 2 per cent.SI