The number of women who bought a home last year rose to nearly match male buyers, despite the persistent gender pay gap and multiple lockdowns during the pandemic, analysis by CoreLogic shows.

During the past year, the share of property purchases by women climbed by 0.9 percentage point to 28.3 per cent from 2020. Over the same period, the proportion of homes bought by men dropped by a similar amount to 29.6 per cent. The remainder of the purchases is by couples.

‘‘COVID-19 and the past year have seen mixed wealth and income outcomes for women, as remote work arrangements threatened to land women with more unpaid carer work, particularly while children were learning remotely, and the health system became more strained,’’ said Eliza Owen, CoreLogic’s head of research.

‘‘Interestingly, however, the past year saw a lot more parity between property sales associated with women and men, which I think could be linked to relatively low concentrations of investor activity, government schemes that help with deposit hurdles, or the increased role of intergenerational wealth in housing where parents help their children do so irrespective of gender.’’

Melbourne-based Mickayla Chapman, who recently bought her first home through ME Bank, said while it took her two years to save the deposit, the financial help from her parents enabled her to buy a two-bedroom, two-bathroom apartment in Reservoir quicker than most people.

‘‘I sacrificed a lot when saving for a deposit and really watched my expenses,’’ she said. ‘‘I was lucky to have my parents help with my deposit, so I could buy sooner.

‘‘It was an overwhelming process, but it was worth it. Buying my home allows me greater freedom, security, and a sense of accomplishment. It’s an asset that could grow in value, but most importantly, a place I could call my own.’’

Ms Owen said the share of properties bought by women had been rising.

‘‘Australia shows a really interesting trend where there’s a marginal shift, year by year, of women purchasing a slightly higher portion of properties, and men purchasing a slightly lower portion,’’ she said.

‘‘This positive trend may start to reflect greater gender parity in home ownership over time.’’

The average loan size for women applying for a single mortgage increased by 7 per cent to $411,752 in 2021 compared with 12 months prior, while the overall proportion of single female applications increased by 1 percentage point to 50 per cent.

In comparison, single male applications rose by 6 per cent to $449,273 in 2021 compared with 12 months prior, while the overall proportion of single male applications fell by 1 percentage point to 50 per cent.

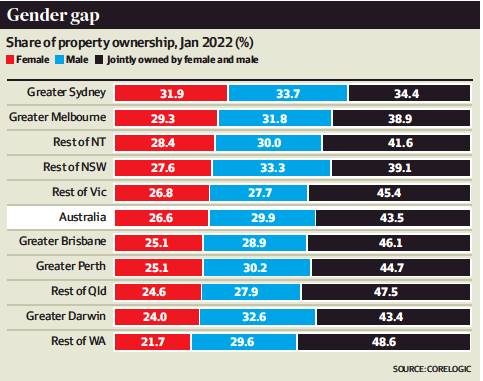

Despite the encouraging trend, the share of home ownership among women has continued to lag men, according to CoreLogic.

Just 26.6 per cent of homes were owned by women, compared with nearly three in 10 (29.9 per cent) owned by men as of January this year.

Milena Malev, CoreLogic International’s general manager for financial services and insurance solutions, said property price increases might have further exacerbated the gender wealth gap in property ownership.

‘‘Given there’s a high level of equity held in real estate, if you don’t own property, that’s a big source of household wealth and security you don’t have access to,’’ she said.

‘‘Property price growth has also vastly outpaced income growth over this time, with the gender pay gap widening in parallel, too.’’

The gender pay gap in full-time ordinary earnings rose from 13.4 per cent at November 2020 to 13.8 per cent in November 2021, according to ABS data. This means men can save the 20 per cent deposit for the current median dwelling value about a year faster than women, said Ms Malev.

‘‘Men are not only accumulating greater wealth from a higher proportion of existing property ownership, but they’re also able to get into the market sooner than women and start that wealth accumulation in a growth market,’’ she said.

CoreLogic also found that men owned 28.5 per cent of all the houses analysed, compared with just 24 per cent owned by women.

‘‘Detached houses generally accumulate more value over time than units, so this essentially accentuates any wealth disparity that comes from housing,’’ said Ms Owen. ‘‘If it continues to widen, then so too would the wealth gap in housing.’’