Home loans Whether you’re an owner-occupier or investor (even via your DIY super fund), you can use these strategies to help handle interest rate rises, writes Duncan Hughes.

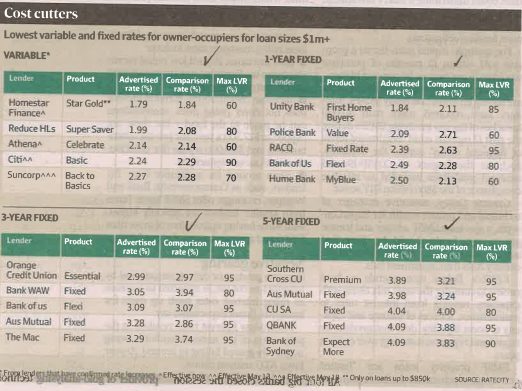

A mortgage-holder with a $1 million home loan on the average variable rate could insulate themselves against the equivalent of several Reserve Bank of Australia cash rate increases by switching to the cheapest variable rate on offer.

It would take more than four rates rises equivalent to this week’s 25-basis-point increase to bridge the gap between the cheapest and average rates on offer, analysis shows.

Before this week’s increase, the average owner-occupier borrower with a 25-year variable rate home loan was paying around 2.92 per cent, or 113 basis points higher than the lowest variable rate.

With lenders passing on the rate rise later this month, the same borrower is expected to pay around 3.17 per cent, or 118 basis points higher than the lowest variable rate on offer.

The lower rate would save a borrower nearly $10,000 in the first year, or $21,500 over two years, according to analysis by RateCity, which monitors savings and borrowing rates.

Bankers warn borrowers there could be a string of interest rate rises over the next year, with RBA governor Philip Lowe saying the cash rate could rise from 0.35 per cent to 2.5 per cent.

The big banks have also updated their cash rate forecasts, with CBA expecting 1.6 per cent by next February and NAB citing 2.6 per cent by August 2024.

A cash rate of 2.6 per cent would mean an increase in monthly repayments of $1350 for a borrower with a $1 million, 25-year principal and interest mortgage.

But other bankers, such as Macquarie bank’s global head of strategy Viktor Shvets, believe deteriorating economic conditions will force central banks to consider ‘‘backpedalling’’ by reducing rates within 12 months.

Mortgage brokers are urging borrowers to ‘‘calmly consider their options’’ and not rush into more expensive alternatives, such as switching from a variable to a fixed rate. Some lenders are increasing fixed rates by more than 50 basis points.

‘‘Borrowers are clearly concerned about the future and how several rate rises will squeeze household budgets,’’ says Phoebe Blamey, director of Clover Financial Solutions, a mortgage broker.

‘‘But many are in a strong position to manage those increases because of increasing savings in offset accounts when rates were low, and a readiness to find a cheaper rate,’’ Blamey says.

Residential property borrowers have made the most of record low rates to squirrel away a record $232 billion in offset accounts (an increase of nearly 15 per cent, or $30 billion) in the past 12 months as insurance against higher rates.

Maile Carnegie, ANZ group executive Australia retail, says around 70 per cent of accounts are ahead on repayments – many of them by two years or more. Household deposits are also at record levels.

Whether you’re an owner-occupier, investor or own a property via a self-managed super fund, here’s how you can lessen the impact of rate rises.

Switch your loan

A borrower with a $1 million mortgage could recoup the costs of switching from the new average variable rate of around 3.17 per cent to the cheapest variable rate on offer within a couple of months.

Costs in switching to a 25-year principal and interest loan would include a $350 discharge fee from the former lender, around $300 in state government fees and upfront fees on the new loan of around $930.

The savings (after costs) of switching from the average to the cheapest variable rate are around $833 a month, RateCity says.

Mortgage brokers warn some nervous borrowers are so concerned about a string of rate rises they are considering paying an extra 100 basis points plus switching fees for the supposed security of a fixed mortgage rate.

‘‘Keep your eye on what is best for your finances,’’ says Christopher Foster-Ramsay, principal of mortgage broker Foster Ramsay Finance. ‘‘Don’t be distracted by guessing what rates will do,’’ he adds.

Some borrowers could be forced to review their borrowing because of changed financial circumstances, such as a job loss or having misrepresented their income, or savings, to the lender. For example, around 37 per cent of homebuyers overstate their financial position when applying for a home loan, according to investment bank UBS. Key issues borrowers need to consider: What rates are on offer and how rising rates will affect repayments and household budget. Can extra repayments be made before the next rate rise? Fees and charges and how long it will take to recoup in lower interest repayments. Breaking a fixed rate can cost thousands of dollars, plus establishment and annual fees with the new lender. Ask for a detailed breakdown before agreeing to the loan, including application, settlement and discharge fees. Some low fixed rates roll to high variable rates after the fixed term, which will also affect the comparison rate.

State government fees vary between states, but expect to pay between $300 and $500.

Check the small print conditions to make sure the loan is portable so could be switched to another property.

What are the loan features? Does it include an offset account and allow additional payments?

Is the lender flexible in case of unexpected events? For example, some lenders offer short-term repayment ‘‘holidays’’. Alternatively, does it accept reduced payments instead of full suspensions, or a combination of both?

Check the level of support, such as call centres, a branch network or internet access.

Too late to fix

Property investors have ‘‘missed the boat’’ for fixed rates and should instead shop around for cheapest variable rates, financial and mortgage advisers say.

An investor with a 20 per cent deposit will pay around 2.59 per cent for a principal-and-interest variable loan from CBA, or around 56 basis points lower than a comparable interest-only mortgage, RateCity says. (These rates have yet to be adjusted following the cash rate rise.)

By comparison, some banks charge 4.39 per cent for a three-year fixed rate or 4.89 per cent for five years.

Alex Jamieson, founder of AJ Financial Planning, says: ‘‘The best time traditionally to fix rates is in the middle of a recession, when interest rates have been cut and the recovery phase is just about to start. That’s not now. Investors considering a fixed-term mortgage have missed the boat. Variable is the way to go.’’

While fixed-rate loans offer some certainty about repayments, they often don’t allow extra payments, are costly to exit and have fewer loan features, such as offset accounts or redraw facilities.

Investors pay a premium of 33 basis points on existing home loans and a 29 basis-point premium on new loans, RBA analysis shows.

Higher rates are unlikely to deter long-term investors seeking higher yields and long-term capital gains, particularly when national property vacancies are less than 1 per cent, the lowest in 17 years, according to SQM Research, which monitors property markets.

Analysts expect rents to rise rapidly in tight rental markets, particularly after the ending of rent caps and eviction controls in the pandemic. These are likely to offset the impact of higher mortgage repayments when rates begin to rise.

Tim Lawless, research director at CoreLogic, which monitors property markets, says while higher rates will discourage some investors, there are others attracted by strong tenant demand, despite low rental demand from foreign students and the soaring cost of building materials and labour shortages.

Every capital city in Australia has vacancy rates below 2 per cent, with Melbourne’s the highest at 1.9 per cent, or less than half what it was about 12 months ago, adds SQM Research.

National gross yields posted a small gain to 3.23 per cent during March, the first since August 2020, and are outperforming capital growth of 2.4 per cent, according to CoreLogic.

As to whether investors are better off on interest-only or principal-and-interest loans, AJ Financial Planning’s Jamieson says a typical long-term investor with a $1 million portfolio is better off paying down the principal and lowering debt using a principal-and-interest loan.

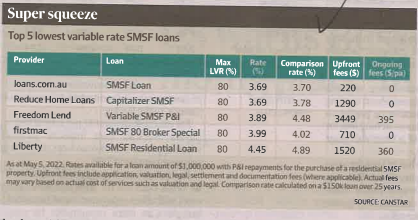

SMSF strategies

Trustees of self-managed super funds (SMSF) investing in property should undertake a full review to ensure there is sufficient liquidity to deal with any financial pressure from rising rates and costs.

SMSF specialists warn increasing expenses might require trustees to increase member contributions, raise rents or sell fund assets to meet increasing liabilities, such as paying pension benefits.

Julie Dolan, head of SMSF and estate planning for KPMG Enterprise, says: ‘‘Trustees should play it safe and have a couple of years’ rental income in the fund as a buffer.’’

Dolan says the likelihood of more interest rate rises over coming months could create stress in funds facing rising expenses without readily available liquid assets, such as listed shares that can be sold, or available cash.

Demand for residential and commercial investment properties jumped during last year’s property boom by around 22 per cent to almost $66 billion, according to analysis by the Australian Taxation Office.

The value of property in SMSFs also rose by about 22 per cent to a record $140 billion, thanks to rising prices and investments, the analysis shows.

Falling property prices and rising interest rates could undermine a fund’s investment strategy and increase taxes if a liquidity squeeze forced a fire sale of a property to meet funding obligations.

For example, capital gains tax on a property sold within 12 months of purchase would be 15 per cent, or 50 per cent higher.

The economic slowdown and rising costs are having an impact on many SMSFs. Auditors have reported more than 40,000 breaches of the law involving SMSFs during the past 12 months amid ‘‘heightened levels of financial stress’’ across the economy, such as the impact of COVID-19 and renewed guidelines intended to increase compliance of the $860 billion DIY sector.

Graeme Colley, executive manager of technical and private wealth for SuperConcepts, a specialist SMSF adviser and trustee group, says funds should be diversified across a range of asset classes to avoid unnecessary risks if an investment fails.

KPMG’s Dolan recommends a fund review to consider the asset mix along with expenses, ranging from interest rates to maintenance, sources of income and capacity to boost liquidity, debt that needs to be repaid and repayment strategy over coming years.

SMSF property loans are ‘‘limited recourse’’, which means the banks can claw back only the specific asset purchased if the loan defaults.

Loan repayments must come from the fund, which means there must be sufficient liquidity or cash flow to meet loan repayments.

Strategies to ensure adequate liquidity to meet rising mortgage rates include:

Rent increases. Record low rental vacancies mean landlords have an unprecedented opportunity to raise rents.

Increase contributions. If rental income does not cover rising rates, contributions can be made to the fund – but these are capped at $27,500 a year (for pre-tax contributions) and $110,000 a year (for contributions with no tax deduction).

Shop around for a cheaper loan. Big lenders, such as Commonwealth Bank and Westpac, no longer offer SMSF loans. Rates from smaller lenders are typically higher, with some having upfront fees of more than $3000 and annual charges of about $400.

Negative gearing

Negative gearing, or debt strategies used by investors to cut tax, is expected to increase as rising interest rates push up costs for landlords, finance specialists say.

Record-low interest rates resulted in the proportion of the nation’s landlords being negatively geared falling to around 20-year lows, ATO analysis shows.

But Shane Oliver, AMP Capital chief economist, says: ‘‘It will probably rise as rates rise.

‘‘The collapse in mortgage rates relative to property rental yields made it harder to negatively gear properties as the interest cost in many cases fell below the property’s net income,’’ Oliver says. ‘‘With rates on the rise again, negative gearing will become easier to achieve.’’

Investor confidence is being partly sustained by the absence of any federal election policies that might lead to a cutback on generous negative gearing concessions or depreciation allowances.

Investors spearheaded demand for residential property loans last year, despite it being difficult to derive much benefit from negative gearing.

‘‘Investors may have been buying in anticipation that the value from negative gearing from a tax perspective will return,’’ Oliver says.

The proportion of Australia’s 2.3 million landlords who are negatively geared was around 60 per cent in 2019, about the same as the previous two years and the lowest since 2003, according to ATO data.

The data shows that in 2019 around 1.3 million landlords made rental losses, while 922,175 (or around 40 per cent) were in a neutral position or made a gain. When losses on an investment property are greater than the gains, the losses can be used to reduce tax on wages or other income.

Analysis by Jeremy Goldschmidt, chief executive of RentBetter, a DIY platform for property investors seeking to cut out professional managers, estimates that average rental properties around Australia are losing their owners more than $1000 a month, despite negative gearing concessions.

Goldschmidt says many landlords fall back on tax deductions rather than looking for more effective ways of cutting expenses and boosting returns.

‘‘Good investing requires close management of expenses. Effective landlords will be looking for ways to manage down other expenses rather than rely on tax deductions,’’ Goldschmidt says.SI