Median house prices fall in 40pc of Sydney suburbs

Dwelling values have dropped in nearly two in five Sydney suburbs during the first three months of the year, while almost half of all Melbourne suburbs analysed posted price declines as the market downturn gathers pace, data from CoreLogic shows.

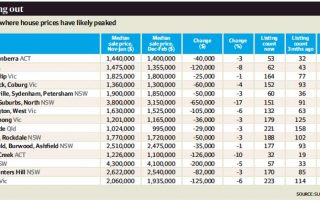

Of the 917 Sydney suburbs analysed, 354 logged a fall in median dwelling values. House prices in 189 Sydney suburbs have slumped, while 165 unit markets weakened during the same period.

In Melbourne, dwelling values across 303 suburbs have dropped during the same period, with 154 house markets and 149 unit markets recording price falls.

Eliza Owen, CoreLogic’s head of research, said the largest price decreases were recorded across some of the more expensive suburbs in Sydney and Melbourne.

Inner Sydney suburbs Beaconsfield, Newtown and Camperdown notched up some of the sharpest house price falls of 7.2 per cent, 5.8 per cent and 5.7 per cent respectively.

In Melbourne, Cremorne posted the largest house price decline of 6.4 per cent, followed by South Yarra with a 4.8 per cent fall and Toorak with a 4.4thper cent drop.

‘‘High-end and inner-city areas are emerging as the first suburbs to experience this shift in market conditions,’’ Ms Owen said. ‘‘It is likely that slightly tighter lending conditions and higher average fixed rates are hitting the very top of housing markets first.

‘‘These same areas are seeing some of the bigger jumps in advertised stock levels too, so as we see new demand for housing in these areas decline buyers have more choice, more time for decision-making, and more power at the negotiating table.’’

Melbourne-based buyer’s agent Cate Bakos of Cate Bakos Property said worries about the rate hikes and global uncertainty were keeping some buyers at bay.

‘‘The constant talk about interest rate increases are making people nervous,’’ she said. ‘‘We’ve also got the federal election, which brings another level of uncertainty, compounded by the war in Ukraine, which are all impacting buyer’s confidence.’’

Sydney-based buyer’s agent Dan Grantham said many Sydney buyers had also pulled back.

‘‘Buyers are not as motivated as they were only a few weeks ago,’’ he said. ‘‘Many have decided it’s best to sit back and wait until after the election and when the first interest rate hike occurs to see how things play out.’’

By contrast, all the 337 Brisbane house markets analysed recorded a rise in median values, and only one out of 171 unit markets posted a decline. In Adelaide, all the 314 house markets in CoreLogic’s analysis racked up price increases and only two out of 105 unit markets fell.

‘‘We’ve already seen a little bit of a slowdown in the rate of quarterly growth across Brisbane and Adelaide, which suggests the rate of growth may have peaked, but I don’t think these cities will move into a decline for quite a few months,’’ Ms Owen said.

‘‘Depending on how the market reacts to a rise in interest rates, we could see these markets slow down around June, when many economists expect the cash rate to rise.’’

In Canberra, dwelling values in seven out of 134 house and unit markets analysed recorded price declines, while six out of 55 house and unit markets across Hobart posted a drop. Across Perth, 13.4 per cent of all suburbs analysed recorded a decline, while 18 per cent logged price falls in Darwin.

As the housing cycle moved into a downswing , more suburbs were likely to record a drop in the median values.

‘‘I think capital growth will be really hard to pinpoint in the context of rising cash rates, but there are markets that could hold much steadier amid a cash rate increase,’’ she said.

‘‘I suspect these will be some of the relatively affordable markets on the periphery of areas that have been popular with internal migrants, such as the hinterland of the Gold Coast or Sunshine Coast.

‘‘I think somewhere like Parramatta in Sydney will be interesting to watch. The ongoing development of infrastructure, people gradually returning to offices, and the return of overseas migration could help to stabilise this market.’’