Distressed home listings jump

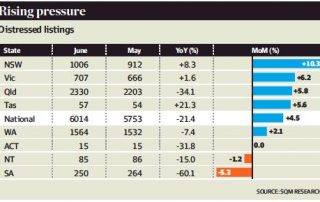

The number of distressed residential listings jumped by more than 10 per cent across NSW in June over the previous month, as vendors struggled to get a sale amid low demand triggered by higher interest rates, poor affordability and rising costs of living, data from SQM Research shows.

Louis Christopher, managing director of SQM Research, said the number of distressed listings would rise to pre-pandemic levels in the months ahead as interest rates lift higher.

‘‘With ongoing rises in interest rates and the end of the COVID-19 relief period within the banking sector, I expect to see distressed listings activity return to levels recorded prior to COVID-19, when it rose to 15,000 nationwide,’’ said Mr Christopher.

More than 1000 homes across NSW were listed under distressed conditions during the same period, with 2330 in Queensland, 1564 in Western Australia and 707 in Victoria.

There were 250 distressed listings in South Australia, 85 in the Northern Territory, 57 in Tasmania, and 15 in the Australian Capital Territory, taking the nationwide tally to 6014 – a 4.5 per cent rise from the previous month.

A distressed residential property listing occurs when a property must be sold quickly, and often results in a financial loss for the seller who must accept a lower price than would normally be the case, said Mr Christopher.

Distressed listings often include key words such as ‘‘mortgagee in possession’’, ‘‘bank forced sale’’, ‘‘desperate vendor’’, ‘‘selling below cost’’, ‘‘must sell’’, ‘‘liquidation’’, ‘‘fire sale’’, ‘‘price reduction’’ and ‘‘motivated vendors’’.

The Gold Coast has the highest number of distressed listings, with 315 homes, followed by the Central Coast in WA with 201, and Queensland’s Sunshine Coast with 185.

A total of 260 properties have been listed as ‘‘mortgagee in possession’’ or ‘‘bank forced sale’’, while 582 were listed as ‘‘bargains’’. Prices were reduced across 1442 listings, while 1426 listings were tagged as ‘‘priced to sell’’ and 1046 were listed as ‘‘motivated sellers’’.

Sydney-based buyer’s agent Jack Henderson of Henderson Advocacy said vendors who had bought a new home but not sold their existing property were the most desperate to sell.

‘‘We’re seeing a rise in these types of vendors, who made large financial commitments and can no longer afford to hold both properties,’’ he said.

‘‘They’re being forced to sell at a price they’re not happy with at all because they don’t have any other options.’’

Amanda Gould, buyer’s agent and founder of HighSpec Properties, said fewer buyers were willing to enter the market as prices continued to drop.

‘‘Buyers are a lot more picky than they have ever been,’’ she said. ‘‘Unless it’s a complete bargain, they’re not interested.’’

The dwindling number of buyers has prompted many vendors to pull out of the market, with new listings falling by 9.4 per cent over the month in Sydney and by 14.4 per cent across Melbourne. Nationwide, listings under 30 days have dropped by 5.4 per cent to 70,885.

But the low absorption rate fuelled a rise in the number of listings over six months, which has lifted by 1.6 per cent nationwide.

‘‘The fall in new listings was a result of reduced vendor confidence in the strength of the housing market, as well as seasonal factors whereby the winter period normally records a decline in residential property sales activity, particularly for Sydney and Melbourne,’’ said Mr Christopher. ‘‘The rise in older listings reveals that the slowdown in the housing market is driven by lower buyer demand. Going forward, we expect July to record similar trends of lacklustre activity and more rises in older listings.’’ Kent Lardner, founder of Suburbtrends, said the rise in inventory was also typically a sign of a market in distress.

‘‘When the balance of power shifts from sellers to buyers, we tend to see a rise in inventory and when this occurs, the time it takes to sell blows out and falling prices usually follow,’’ he said.

‘‘Right now, inventory is rising in 60 per cent of housing markets and in 50 per cent of unit markets.

‘‘If inventory levels build to more than five or six months, that is where I expect to see double-digit price changes.’’