Surging rents add to supply concerns amid tax changes

Rents are accelerating at their fastest pace in 2½ years and are likely to rise further, amid concerns the federal budget will do little to boost housing supply in the short term and may even add to the cost of renting.

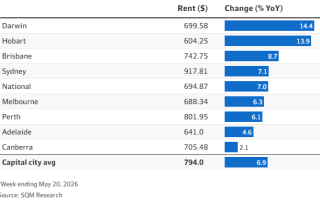

Weekly asking rents across the capital cities rose an average 6.9 per cent from a year ago, SQM Research figures on Wednesday showed, with the combined figure for houses and units in Sydney up 7.1 per cent year-on-year, up 6.3 per cent in Melbourne and 8.7 per cent in Brisbane.

The yearly rate of gain is likely to go as high as 10 per cent over the next year – putting it above the 9.2 per cent chalked up in November 2023 – as the underlying shortfall of rental houses is exacerbated by last week’s federal budget, leading to a reduction in rental housing supply, said SQM managing director Louis Christopher.

“I’m seeing no change with building numbers or suggestions there will be equilibrium between supply and demand any time soon,” he said.

“Going forward with the property tax changes, we can expect a decline in available rental stock over the course of the next two years. Rental yields will need to rise to encourage investors back into the market and that will happen through a combination of housing price falls and rises in rents.”

The budget announcement that negative gearing and the 50 per cent discount on nominal capital gains will no longer be available to investors for existing homes – although they both remain available for investment in new builds – has stoked debate about the extent to which the tax breaks subsidise rents.

Investor advocates have said negative gearing – which allows a landlord to offset losses from a rental property against other forms of income, such as wages – keeps rents lower than they would otherwise be.

“Rents are a persistent inflation … That 7 per cent you have today is embedded in 6 months’ time. There’s almost nothing you can do about it.”

“Anything that eases their investor cash flow enables them to hold a property,” said Cate Bakos, a buyers’ agent and chair of industry body Property Investment Professionals of Australia.

“It’s a crude way of putting it, but it certainly subsidises rent. It alleviates their holding costs.”

That was seen during the COVID-19 pandemic when lower interest rates made it easier for landlords to accept rental reductions or freezes, Bakos said.

“It was far easier to say ‘yes’ because holding costs were less,” she said.

Independent economist Saul Eslake said, however, that rents were set more by vacancy rates and what the market would bear, rather than costs faced by landlords.

“Rental is not a cost-plus business,” he said. “That is, landlords charge what the market will bear, which is driven largely by vacancy rates.”

Rents did not fall last year when the Reserve Bank of Australia was cutting interest rates and they had not risen this year as a result of borrowing costs rising again or because council rates rose for landlords, he said.

Rather, negative gearing had allowed landlords to borrow more to push up prices, Eslake said.

“By incentivising landlords to borrow more money to bid up, forcing up the price of housing we’ve already got, they’ve inflated the price of housing,” he said.

“If negative gearing didn’t exist property prices wouldn’t be as high as they are and rents as a percentage of the cost of property wouldn’t be higher, either. Landlords wouldn’t need to raise rents as much to make a return on their asset.”

Higher rents do raise risks for inflation. Christopher said the near 7 per cent capital city annual rate of increase for rents was the highest since the post-pandemic period.

Barrenjoey chief economist Jo Masters said rents made up the second-largest line item in the official CPI basket – after the cost of building a new home – and that the trend of rising rents was a risk.

The CPI rental figure represents the so-called stock of all rents – that is, all rental prices, whether they are renewed or not – so it will be lower than the current rise in asking rents.

But Barrenjoey’s forecast this calendar year is for 3.9 per cent CPI rent inflation, which Masters said was “quite strong”.

“Rents are a persistent inflation,” she said. “That 7 per cent you have today is embedded in 6 months’ time. There’s almost nothing you can do about it.”

Bakos said when investors were pressured financially they would push to get the highest rent they could.

“We’ve seen it with land tax; we’ve seen it with increased interest rates,” she said.

Christopher said the post-pandemic acceleration of rents, which have jumped from a yearly growth rate of 2.5 per cent in May last year to 6.9 per cent now, would put pressure on headline inflation.

“Is it a return back to the days of 2021 and 2022? Not yet, but it’s clear the re-acceleration will feed into the Australian Bureau of Statistics’ CPI soon,” he said.