Former RBA economist slams bank’s pandemic response

The Reserve Bank damaged its credibility by miscalculating the inflationary effects of the pandemic, acting too slowly to tame rising prices and poorly communicating its intentions to the market, according to a former RBA senior economist.

Jeremy Lawson, chief economist for UK-based fund manager abrdn, which last year rebranded from Standard Life Aberdeen, where he also heads its research institute, worked at the RBA for seven years until 2008.

The RBA has echoed errors from other central banks around the world, notably the Federal Reserve, in waiting too long to act to temper swiftly rising prices, he said.

‘‘The credibility of the RBA has been damaged,’’ Mr Lawson told AFR Weekend. ‘‘Central banks really misdiagnosed just how this pandemic would influence the inflationary environment.’’

Among the RBA’s biggest mistakes has been its communications, according to Mr Lawson, who is the latest in a line of economists to criticise the bank for claiming that rates were unlikely to rise until ‘‘2024 at the earliest’’ in monetary policy statements.

‘‘They were obviously trying to underpin confidence that rates would remain low for an extended period of time, especially early in the pandemic, but it came across as a promise,’’ he said. ‘‘That communication was too strong in an uncertain environment.’’

The idea that rates would remain near zero for years may not have convinced professional investors, but everyday borrowers may have loaded up on debt that will become increasingly difficult to service as interest rates rise.

‘‘It’s one thing for markets to be thrown around by these things, but individuals, they make day-to-day decisions based on things that they might get in a headline,’’ he said. ‘‘If [rates increase] rapidly, that can have really foul consequences for people.’’

Mr Lawson’s comments come weeks after RBA Governor Philip Lowe admitted the central bank’s pandemic guidance that interest rates would not rise until at least 2024 was an ‘‘embarrassing’’ error and it ‘‘should have done better’’.

Dr Lowe said an internal RBA review of its so-called forward guidance during the pandemic would be conducted and findings made later this year.

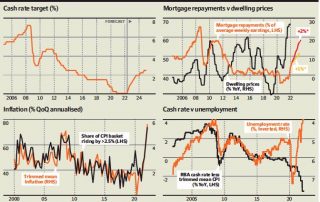

Next week, the central bank is set to increase rates for just the second time since 2010 after last month’s 25-basispoint increase that lifted the cash rate to 0.35 per cent from its pandemic level record low of 0.1 per cent.

Economists are divided on whether the bank will raise by a further 25 basis points when it meets on Tuesday or push through a more aggressive 40-basis-point increase that would bring the rate to 0.75 per cent.

Mr Lawson said the RBA should move aggressively to tame the swift increase in consumer prices in the same vein as central banks in the US, Canada and New Zealand, which have each increased rates by 50 basis points this year. ‘‘It’s increasingly likely they’ll go in larger jumps, which is the right thing to do. Then, depending on how the economy, the housing markets, and how forward indicators evolve, maybe they can justify a pause.’’

‘‘[If they] go at 25, 25, 25, then they only get to where they need to be sometime in 2023. That’s taking too long.’’

He thinks the Australian cash rate will peak at 2.75 per cent in the current hiking cycle, a forecast roughly in line with three of the four major banks.

Commonwealth Bank remains an outlier: its economists expect a shallower tightening cycle with a terminal rate of 1.6 per cent early next year. Investors hold a more bullish outlook, however, with bond market pricing implying the cash rate will increase to 3.6 per cent over the next 12 months.

The global wave of rising interest rates across developed market economies to dampen inflation will increase the likelihood of recession in the coming years, which has become abrdn’s base case scenario.

{kind=link}

{kind=link}