Financial risk warning as more home owners struggle

Home loan hardship applications jumped ‘‘materially’’ in the past year, and the risk posed to the economy by stretched borrowers ‘‘warranted ongoing close attention’’, the regulatory group in charge of the financial system urged.

The Council of Financial Regulators said there was an increase in ‘‘the share of households who had fallen behind on loan payments’’ and that its members – the Reserve Bank, Treasury, banking regulator and market regulator – ‘‘expect some further increase in the period ahead’’.

Loan arrears advanced at their fastest for at least two years in January, from historically low levels.

‘‘Hardship applications had risen materially over the past year,’’ the council said in its quarterly statement issued yesterday. ‘‘Risks to the Australian financial system from lending to households warranted ongoing close attention but remain contained.’’

The council said the risk to broader financial stability hung on the outlook for inflation and unemployment.

‘‘Risks to household balance sheets, and in turn financial stability, would increase if inflation were to remain high for longer than anticipated or if labour market conditions deteriorate more than expected,’’ it said.

The jobless rate ticked up to 4.1 per cent in January, from 3.9 per cent in December.

The council said bank lending standards remained sound ‘‘despite the competitive lending environment’’, which is heating up again with a rise in below-the-line discounting.

Banks increased their provisioning for bad loans, last month’s profit updates revealed.

National Australia Bank, for example, said credit impairment costs rose 17 per cent to $193 million in the December quarter. Westpac announced a $189 million impairment charge for the first quarter, 47 per cent higher than the second half average.

Ninety-day arrears – the most at risk of default – rose 9 basis points to 0.95 per cent at Westpac in the October-December. At NAB, the number was steady at 0.75 per cent of its home lending book.

‘‘The last leg of this tightening cycle could prove to be the most challenging, as savings are depleted, unemployment rises, and higher interest rates continue,’’ S&P warned last month.

The council also said that, despite the challenging conditions in commercial real estate, the risks were contained ‘‘due to banks’ low exposures, conservative lending practices and the relatively strong financial positions of . . . owners’’.

Stress in overseas commercial real estate may, however, bleed into Australia because of the concentration of foreign ownership in the local sector, and the council said it would continue to monitor the situation.

It also stressed the importance of government and industry collaborating to ‘‘ensure the sustainable arrangements or cash distribution in Australia’’ as the only major distributor, Lindsay Fox’s Armaguard, warned it needs more funding to stay afloat.

NSW tops states with the highest rent increases

Surging rents fuelled by housing supply shortages have pushed rental affordability to its worst level in 17 years and will keep pressure on inflation for some time yet, a new report warns.

Lower-income households are being hit hardest by rising rents, and the poorest fifth – those earning $49,000 per year or less – would need to pay more than 25 per cent of their pre-tax income for any advertised rental, data company Proptrack said. It defines affordable rent as accounting for less than 25 per cent of a household’s pretax income.

The rate of rent increases was expected to remain high in an undersupplied housing market, making it even tougher for the Reserve Bank to bring inflation back to the middle of its target range, Proptrack senior economist Angus Moore said.

‘‘The rapid pace of rent growth we’re seeing has been adding to inflation, particularly since rents are quite a sizeable part of the CPI basket,’’ Mr Moore said. ‘‘Given that advertised rent growth has been quite strong, and tends to lead growth in average outstanding rents, we’re likely to continue to see rents making a solid contribution to inflation for a little while yet.’’

Rent inflation hit a decade high of 7.8 per cent last year and has remained above 7 per cent since, Australian Bureau of Statistics data show. This has meant rent’s proportion of the CPI basket grew 6.03 per cent in January, an increase of 28 basis points from the same time last year.

Rents surged 11.5 per cent in calendar year 2023 after growing 15.6 per cent in 2022, Proptrack data show. To start 2024, national median advertised rents have risen to $600 a week from just over $400 in 2020.

Rents at the most affordable end of the market have increased by 43 per cent in the past five years, compared to 30 per cent for the most expensive rentals. This equates to a 10th percentile rental going from $280 per week in 2018-19 to $400 today.

Mr Moore called for more rental support for low-income renters such as Commonwealth Rent Assistance, following similar calls from developers, think tanks and housing groups in recent months.

‘‘Without support, renting would be impossible for many of these households given their incomes,’’ he said.

Grattan Institute’s Brendan Coates in January urged the Albanese government to increase funding for the rent assistance scheme by 22 per cent, on top of a 15 per cent rise in last year’s budget.

It’s not just the poorest households struggling with affordability, as median-income households could only afford four out of 10 advertised rentals compared to being able to afford 60 per cent of listings three years ago.

NSW was the least affordable state for renters. Rental affordability has deteriorated significantly in NSW over the past three years and is at its lowest-ever level after median rents rose to $700 a week. As a result, a median-income NSW household can only afford to rent about three out of 10 properties advertised.

This was followed by Tasmania and Queensland. In Tasmania, a household earning median income for Tasmania – equivalent to approximately $79,000 per year – could only afford to rent one in five advertised rentals, the lowest share of any state.

Queensland rents, meanwhile, have surged 45 per cent in three years, leading to a median income household for the state – about $107,000 – only being able to afford three of 10 properties advertised across the state.

Victoria was the most affordable state when comparing rents to residents’ incomes, due to its rents declining the most during the pandemic lockdowns and more homes being built relative to other states. A median-income Victorian household can afford more than 50 per cent of listings.

Why Australia needs an institute for applied ethics

Capitalism depends on government to provide a trusted framework of rules around it. But when politics turns into reality TV, we must ask the ethical questions ourselves.

The capitalist model, detailed in Milton Friedman’s 1962 classic, Capitalism and Freedom, is often criticised by non-economists for celebrating the pursuit of self-interest.

Yet capitalism’s claims to moral legitimacy come not only from its promotion of liberty, but also from its impressive claims to aggregate economic efficiency. Specifically, capitalism claims to produce community outcomes that are Pareto optimal, meaning that no one person can be made better off without at least one other person being made worse off.

Except as required by the law of the land, individuals in a capitalist system are not obliged to attend to the interests of another. They are free to pursue persistently divergent interests, as workers, investors and consumers. And those who run businesses have no social responsibility beyond the pursuit of profit.

But while the capitalist model is founded on the pursuit of self-interest, it will not function in the absence of trust. Mutual confidence in the functioning of the capitalist system is critical to its claimed efficiency benefits. A lack of trust means a suboptimal number and size of transactions, and underinvestment in innovation, with significant implications for the level of aggregate economic activity, productivity and real income growth. Moreover, a sudden loss of trust can have catastrophic social consequences, as the global financial crisis of 2008-09 illustrates.

A recent report by Deloitte Access Economics, commissioned by The Ethics Centre, explains how large gains in economic activity can be achieved with modest improvements in levels of trust.

Readers of this newspaper have observed how trust in business has been undermined by apparent failures to meet community expectations in the treatment of customers in many sectors of the economy, including through impenetrable information disclosures, automated customer call centres and store closures. And, like all other Australians, they would be wondering about their capacity to cope with the many ways in which businesses and governments might make use of advances in AI and robotics.

In the capitalist system, businesses are not to concern themselves with meeting community expectations, except to the extent that doing so increases profit. Ensuring that business meets community expectations is the responsibility of government.

As Friedman puts it, capitalism relies upon a functioning democratic system that both enables and obliges its citizens to elect governments to ‘‘determine, arbitrate and enforce . . . a framework of law’’ to ensure ‘‘free and open competition’’ and protection from ‘‘fraud or deception’’. And Friedman goes on to explain, if somewhat grudgingly, that government also has responsibility for attending to negative externalities and making adequate provision of public goods.

Capitalism casts business and ‘‘the rest of us’’ (Friedman’s expression) as adversaries, and government as our protector.

So, it is something of a paradox that, year after year, surveys of ‘‘the rest of us’’ report that, among the principal institutions affecting our lives – businesses, not-for-profit entities, government and the media – it is government that enjoys the least trust.

Capitalism demands a lot from government. Mostly, our political leaders fall short. Instead of attending to frameworks of law and enforcement, many have preferred the role of business-bashing critic, pointing an accusatory finger at business executives, not themselves, for having failed the pub test or for failing to meet community expectations.

It may be the case that the 24/7 reality TV show, through which citizens get to observe the workings of modern politics, encourages this sort of spectacle.

Yet, no matter its explanation, it is corrosive of effective governance, which depends upon elected officials having some detachment from outrage and mania, not seeking energetic immersion in it.

We have a problem.

Following the global financial crisis, serious thinkers around the world began questioning whether the adversarial contest at the core of the capitalist system might not be its Achilles heel.

Capitalism proposes a system in which business is motivated by nothing other than profit, and its executives by nothing other than self-interest, and leaves it to the rest of us, also motivated by nothing other than self-interest, to elect politicians to protect us with laws that we cannot possibly comprehend and regulatory bodies with which we can have no meaningful contact. This is not an arrangement designed to build trust.

Recent global efforts to make more transparent the social and environmental impacts of business activity, and to have business leaders accept accountability to the community for these impacts, seem to me to be steps in the right direction.

But these will only take us so far. The big problem we have is that, as individuals and as a community, we confront a set of ethical questions that are just damned difficult. And we have not invested sufficiently in respected institutions that might help us think them through.

In all democracies, there is a compelling case for centres of expertise that facilitate sober reflection. This is why we fund universities, a professional public service and, within the public sector, institutions that enjoy a higher level of independence, such as the CSIRO and the Productivity Commission.

Yet, when you reflect on the recent and emerging causes of a loss of trust in democratic capitalist systems, and the economic and social gains that would come from addressing them, you have to think that something is missing. That is why I have come to the view that it is time for us, as a community, to invest in an Australian Institute for Applied Ethics. This is a modest investment, promising very large rewards.

Ken Henry is a former Treasury secretary, and one of 1600 signatories of an open letter calling for federal funding for an Australian Institute for Applied Ethics.

No quick fix for housing problems

If it wasn’t already very clear, yesterday’s big miss on building approvals is more evidence that the thorny problem of increased supply in the housing market won’t be solved anytime soon.

The latest data was so bad – the 1 per cent fall in January took building approvals to a 12-year low, and detached dwellings were down 9.9 per cent in a month – that it probably should be treated with a grain of salt; there seems to be a lot of seasonal noise in economic data at the moment.

Still, when we take yesterday’s numbers alongside last week’s residential construction data, which showed the pace of home building is slowing (from an annual rate of 11.4 per cent in the middle of last year to just 0.7 per cent in the December quarter) then the federal government’s hopes of building 1.2 million homes in five years already start to look distant.

And of course, with supply still weak and demand from population growth strong, it’s no surprise that house prices are gaining steam again. The latest CoreLogic house price data showed prices in February rose 0.6 per cent month-on-month, up from an average of 0.3 per cent in the previous three months. Auction clearance rates have been stronger in the past four weekends than in late December 2023 and Domain’s latest data showed a record low for the national rental vacancy rate.

HSBC’s local chief economist, Paul Bloxham, forecasts house price growth of 3 per cent to 6 per cent across the year, predicting the construction sector’s struggles will limit supply, strong employment will limit distressed sales and arrears, and the demand impulse from population growth won’t fade quickly.

But while the wealth effect from higher house prices – and indeed a local sharemarket that keeps eking out fresh records every few days – might warm the cockles of the hearts of Australian households, Bloxham wonders if there’s another side-effect we need to start considering: rising house prices and higher rents are not typically a recipe for RBA rate cuts.

He sees three key concerns.

First, renewed growth in house prices may be taken as a sign that the household sector is holding up reasonably well in the face of 13 official rate increases. This column would throw the rise in equity markets (which will flow through to higher retirement payouts and higher savings) as further evidence that financial conditions actually look pretty good. Clearly, the ‘‘average’’ experience across the economy masks some real pain out there among younger, more indebted households, but the RBA cannot set rates for this cohort alone.

Second, Bloxham says the RBA will be rightly wary that an undersupplied housing market will mean rents remain a strong contributor to inflation. Governor Michele Bullock has repeatedly raised concerns about the stickiness of services inflation, and rents are the key challenge here.

Third, Bloxham argues that the RBA may be wary of ‘‘pump-priming a housing market that is already heating up’’ by delivering rate cuts. ‘‘In short, there is some circularity in current events, as expectations for rate cuts may be fuelling a housing price rise, but, at the same time, the housing price upswing may be making those rate cuts less likely. Our central case is that rate cuts are unlikely in Australia in 2024.’’

We’ll get another piece of the rates puzzle tomorrow, when December quarter GDP data is released. Consensus is for growth of 0.3 per cent quarter-on-quarter and 1.5 per cent year-on-year, but economists unanimously raised the prospect of a negative reading after other economic data released yesterday showed a substantial drop in inventories across the economy.

With productivity stuck in low gear and the employment market still strong, weaker GDP growth is needed to bring down inflation. But Bloxham says the undersupply in the housing market is evidence that the economy is probably ‘‘still operating beyond its sustainable rate’’. And that may make it harder for the RBA to cut.

Another factor for the RBA to watch is the Federal Reserve’s view on rate cuts. Softer economic data out over the weekend has prompted traders to adjust their bets such that markets now expect the Fed will cut rates by 86 basis points in 2024, from 77 basis points last week. It’s worth noting that the year began with markets expecting 150 basis points of cuts.

Torsten Slok, chief economist at US private capital giant Apollo Global Management, now predicts no cuts in 2024, as strong consumer spending, strong investment by companies and a strong labour market keep inflation sticky. Clearly, financial markets see this as an extreme view. But if the Fed was to stay on hold, the RBA may be even more confident about following suit.

Avenue prevails after APRA raised banking bar

Avenue Bank has been awarded an unrestricted banking licence by the Australian Prudential Regulation Authority and will become the country’s first niche bank focused on providing bank guarantees to small businesses and landlords.

‘‘We are the first and only bank to specialise in bank guarantees, and we are hopeful there will be strong take-up of the product this year,’’ said Avenue Bank CEO Peita Piper.

APRA gave it the green light yesterday.

Avenue will target the $9 billion of deposits held under bank guarantees provided by tenants renting from commercial landlords. The average bank guarantee is $125,000. By winning just 2 per cent of the $9 billion market, Avenue says it can break even.

Avenue will look to attract business off the major banks from big leasing agents including Colliers, CBRE, Knight Frank and Ray White; large commercial landlords like Dexus, Mirvac, GPT and Scentre Group; and tenant advisers such as Franklin Shanks and Kernel.

‘‘The current bank guarantee procedures are onerous, paper centric, and cause issues for small businesses and landlords, as they can take four to six weeks,’’ Ms Piper said.

‘‘We have digitised the process and can do them in 24 hours, with a five-minute application. And this is just the start of what we are doing.’’

Avenue also has plans to launch, within a year, a drawdown facility on its deposits, to allow tenants to free up working capital.

Avenue is the second new bank to be fully licensed by APRA after the high-profile failures of two neobanks, Volt and Xinja, both of which had targeted retail deposits and lending.

Alex Bank, a personal lender, won an unrestricted licence in December 2022. Avenue has been operating under a restricted authorised deposit-taking licence granted in September 2021.

Ms Piper said the collapse of Volt and Xinja, and the failure of several US lenders last year including Silicon Valley Bank, had raised APRA’s bar for new entrants.

‘‘It’s been a very thorough and rigorous process,’’ she said. ‘‘The bar kept getting higher and higher. The fact we have got through COVID, and the collapse of neos and some American banks, in a dire equity [raising] market is testament to our strength.’’

The market opportunity for Avenue has been created because commercial landlords force tenants to put up between nine and 12 months of rent to provide the landlord with funds should a tenant’s business fail, or if it breaches a rental agreement.

Avenue will write term deposits, paying 3.5 per cent to the tenant, and issue the guarantee digitally to the landlord or property owner. Under its restricted licence, it has been able to take on 14 customers, including Tank Stream Labs, which provides working space for start-ups, to test its systems and procedures.

Initially, Avenue will take no credit risk. It will make money by investing the deposits, returning more than what it pays out in interest. The spread will be around 1 per cent.

When interest rates fall, the margin is managed by reducing term deposit rates in lockstep with bond yields. It will also earn a fee of 3 per cent of each guarantee written.

Ms Piper said major banks, which also issue the products, were not likely to respond with better processes ‘‘because bank guarantees are not a priority for them’’.

The plan is to then add features, including allowing tenants to withdraw 90 per cent of their deposits to free up cash flow. This will involve Avenue taking credit risk on the tenant’s ability to meet the conditions in the lease. It will also offer other tools for landlords to manage claims on guarantees.

Non-bank mortgage lender Liberty Financial Group is a major shareholder of Avenue, which has just completed a series D capital raising for $17.7 million. This brings total equity raised since 2021 to about $70 million; it plans to raise more to fund its expansion.

Xinja failed in late 2020 because it started paying interest to savers before making loans on which it would earn returns, evaporating funding. Volt Bank was forced to close and return its deposits in mid-2022 after it failed to get enough funding.

APRA slowed down the timetable for Avenue’s licence, to get satisfied it had sufficient resolution plans setting out how it would exit the industry were it to fail, a requirement for all banks.

Avenue’s co-founders were Colin Porter and Dale Hurley, who set up CreditorWatch in 2011 and cracked the credit reporting agency duopoly before that business was sold in 2017.

On the 2 1/2 years it took Avenue to get its full licence from launch, Mr Porter said: ‘‘APRA don’t like seeing a bank application from a bunch of disruptive entrepreneurs with an innovative product. That has been the challenge, and that is something they will need to get their head around if more banks will be starting.’’

Tax rise ‘last nail in the coffin’: agent

Property manager Carmen Littley says she has lost 52 investor clients since the Victorian government targeted landowners with extra levies in its budget last year, which she describes as the ‘‘final nail in the coffin’’ for many owners.

She warned that property investors leaving the market would further hit rental stock because owner-occupiers tend to have fewer people in a house than renters, which could potentially further increase asking rents.

Land tax increases piled up alongside the fastest interest rate rising cycle in a generation and local government rate rises, said the agent, who is based in the western suburb of Werribee.

‘‘There’s no incentive to invest in property in Victoria,’’ Ms Littley said. ‘‘Landlords have been targeted to pay off the state’s debt, so it’s a no-brainer. The land tax increases were the final nail in the coffin.’’

Victorian Treasurer Tim Pallas last year said the COVID-19 debt levy would hit ‘‘those most able to pay’’, extracting $4.7 billion from property investors over the next four years, along with $3.9 billion from businesses with payrolls above $10 million.

Landowners would pay an average of $1300 in extra land tax, although tax experts said the change equated to a $1675 increase on land worth $1 million. Family homes are exempt. Economic research organisation e61 released a report this year showing Melburnians face the highest stamp duty in Australia.

The tax slug, which hit 380,000 additional landowners, will raise $4.74 billion over the forward estimates by cutting the tax-free threshold for land tax from $300,000 to $50,000, imposing new yearly flat fees and increasing the rate of tax payable on properties over $300,000 by 0.1 percentage point.

One of Ms Littley’s clients, Marcel-line Parker, moved to sell her two-bedroom investment unit in Werribee this week after receiving a land tax bill for $975 on her property which had total taxable value of land of $112,000.

‘‘The land tax was the final blow. Just because you have an investment property, it doesn’t mean you’re loaded,’’ the office administration worker said.

‘‘The state government has us by the you-know-what. It’s not worth it.’’

Geoff White, a real estate agent for Barry Plant with a focus on apartments at Melbourne’s Docklands, estimated that half of investors selling out were doing so because of ‘‘unsustainable’’ costs including land taxes and owners’ corporation fees.

CoreLogic research director Tim Lawless said 31.7 per cent of new mortgages written in December in Victoria were for investors, which was below NSW at 40.7 per cent, and the national average of 36.2 per cent.

In addition to higher land taxes in Victoria, other cities such as Perth and Brisbane offered higher yield, better growth and lower buy-in prices for investors than Melbourne, he said.

‘‘There is absolutely a risk of flight from Victoria,’’ he said.

Property Investments Professionals of Australia director Richard Crabb said the industry body’s annual investor sentiment survey released in September showed Victoria was the least attractive state for investors in the nation. It also found that 25 per cent of respondents sold at least one investment property in Melbourne in the 12 months to August last year — the worst of any capital city.

Record number of borrowers at risk of mortgage stress, report says

Borrowers in Western Australia are 20 per cent more likely to fall behind on their mortgages, according to S&P Global Ratings, which found home loan arrears rose in the December quarter and are likely to worsen.

While overall major bank arrears remain low – averaging 0.91 per cent of loans across the economy – the Reserve Bank’s 13 interest rate increases and its 4.35 per cent cash rate are starting to bite. Roy Morgan, in a separate report yesterday, found a record high 1.6 million people, or 31 per cent of borrowers, are at risk of mortgage stress.

‘‘The last leg of this tightening cycle could prove to be the most challenging, as savings are depleted, unemployment rises, and higher interest rates continue,’’ S&P Global Ratings said.

‘‘Financial prudence might no longer be enough for some households, leading to further increases in arrears in the months ahead.’’

At its interim results this month, Commonwealth Bank said it was supporting more than 7000 home loan customers in formal ‘‘hardship’’, including providing options to suspend mortgage repayments or to move to interest-only repayments.

That came as CEO Matt Comyn indicated that the first official rate cuts might not materialise until next year.

Borrowers who are not making repayments appear to be staying in their homes for longer than in past economic cycles, as banks seek to minimise the scrutiny that comes with calling in their loans, says Field Research director Stewart Oldfield.

In the biggest markets of NSW and Victoria, mortgage arrears are stable. In NSW, the proportion of borrowers more than 30 days late on repayments was 0.96 per cent in December from 0.94 per cent in July 2023 and 1.01 per cent in November.

But in WA, more borrowers are behind: 1.19 per cent are more than a month overdue, although this had improved from 1.50 per cent in July last year. The best performing state is Tasmania, at 0.48 per cent.

CBA this month said official rate rises were being unevenly felt, as savings were depleted faster for younger borrowers. Savings of customers aged between 25 and 34 were down 2.4 per cent year-on-year and for the 35 to 44 band, savings were 2.1 per cent lower. They rose for over 65s by 6.5 per cent.

Roy Morgan said the number of mortgage holders considered ‘‘at risk’’ of mortgage stress had surged to a record on the back of the Melbourne Cup Day rate rise in November. The 1.6 million at risk – defined as borrowers who allocate between 25 per cent and 45 per cent of their after-tax income to repayments – has increased by 802,000 since May 2022, when the RBA began tightening.

If the central bank raises rates by a further 0.25 percentage points next month, this will push a further 16,000 borrowers into the risky category, the group estimates.

The number of mortgage holders considered ‘‘extremely’’ at risk – allocating more than 45 per cent of their income – is now almost 1 million, or 19.8 per cent of borrowers. The average over the past decade is 14.3 per cent.

NABank last week said its quarterly cash earnings had dived by 16.9 per cent amid an economic slowdown, reflected in rising mortgage arrears and a $193 million impairment charge.

Scandal-ridden finale for ATO boss Jordan

Taxing times PwC scandals and GST frauds are casting a long shadow, but the commissioner points to his successes, writes Jennifer Hewett.

Chris Jordan leaves his high-profile role as tax commissioner dodging another hail of political brickbats but confident he has delivered much better service and a digital revolution at the ATO – as well as forcing multinational companies to pay billions more in tax.

That’s despite the finale of his 11 years dominated by the politics of the PwC tax scandal and, just this week, criticism from the auditor-general of the ATO’s response to a giant GST fraud scheme that went viral on TikTok.

Not only were 12 officials working at the Tax Office and around 140 other former ATO contractors and employees among the tens of thousands of Australians investigated or charged, the auditor-general also found the agency’s internal risk framework was lacking.

This requires Jordan to belatedly acknowledge the failure of the ATO’s systems when ‘‘57,000 people trying it on meant the GST scam got out of control’’. Banks suspicious about their customers’ behaviour finally raised the issue with the Reserve Bank.

But as Australia’s 12th tax commissioner prepared for his last personal grilling at Senate estimates on Wednesday afternoon, he sounded his typically forthright self.

As evidence of the positive change at the ATO, he cites the Public Service Commission’s annual report measuring trust in Australian public services. This shows the chief revenue raising body in the country had one of the highest ratings of any government department or agency last year – equal third with Parks Australia.

‘‘And we’re the ones that take money from people,’’ he says happily. ‘‘The ones that give money out are way down the scale.’’

He still has to concede the response to the GST scam could have been better, insisting it will be, ‘‘now that we know the appetite of the community to do such large-scale fraud’’.

The ATO has established a new fraud and criminal behaviour unit to combat the new normal in a digital world, including surging industrialised identity theft.

For Jordan, it’s also about the ‘‘tension that exists between providing client service and putting grittiness in the system to stop fraud’’.

That service element included the requirement on the ATO to repay GST refund claims within 14 days, for example, making it more difficult to investigate potential fraud until after the money had been paid.

That’s particularly fraught in an agency which he maintains ‘‘falls over backwards’’ trying to help small businesses, including with timely registrations for Australian business numbers and GST refunds.

He still appreciates that the auditor general’s report and the continuing PwC fallout will overshadow, at least temporarily, one of his proudest achievements – ‘‘the cultural transformation’’ of the ATO.

In his office overlooking Barangaroo in Sydney, Jordan brings up the ATO app on his mobile to demonstrate the ATO’s ‘‘contemporary’’ approach under his leadership. It’s a spectacularly slick, easy-to-use comparison to the struggling, inadequate efforts by other departments to digitise federal government services, including via the clunky myGov app.

‘‘I think not having grown up with the rules and regulations of the public service enabled me to challenge things that I just thought were silly or unnecessary,’’ Jordan says.

‘‘A lot of senior public servants have what I call passive resignation to the

status quo . . . they don’t seem to have a passionate desire to get rid of unnecessary complexity in their own organisation.’’ What will happen at the ATO from now on is less clear.

Jordan came to the Tax Office from KPMG: the first private sector player to become Australia’s tax commissioner; the first to live in Sydney rather than Canberra; the first to engage so enthusiastically in vigorous public debate about the need to firmly combat behaviour and corporate structures designed to avoid tax.

Will he be the last of his type?

Treasurer Jim Chalmers, for example, has restored the ATO tradition of appointing a senior, long-term public servant to the role, naming Rob Heferen as Jordan’s replacement from March 1. Heferen was chosen over deputy commissioner Jeremy Hirschhorn – whom Jordan had also brought over to the ATO from KPMG and had been widely expected to become his replacement.

Chalmers’ choice followed months of revelations in The Australian Financial Review about PwC’s activities turning into fiery political theatre in the Senate. Greens and Labor senators probed – with dramatic effect – the extent of PwC’s betrayal of its obligations and how aggressively the ATO had pursued this over several years.

Jordan and Hirschhorn found themselves in the political firing line even as they insisted that their jobs required them to obey the draconian secrecy provisions of the Tax Act.

The tax commissioner certainly believes the reaction – which intensified Labor’s pre-election commitment to curb the use of consultants – affected Hirschhorn’s chances of appointment to the role of tax commissioner.

‘‘Obviously, the Treasurer knew Rob Heferen because he was working in Wayne Swan’s office when Rob was head of the revenue unit at Treasury,’’ he says cautiously. ‘‘But I have no doubt it (the PwC issue) would not have helped Jeremy because he had been widely seen as the frontrunner.’’

He also argues the increasingly personal nature of some of the political attacks will make the idea of transferring between the private and public sectors less appealing to other senior business figures.

But Jordan himself has always understood the vicissitudes of the political world extremely well due to decades of working closely with politicians on both sides.

After starting his working life as a young copper, Jordan shifted to study accounting. His CV ever since is a microcosm of the circles within circles in Australia’s leadership positions.

Originally drafted from KPMG to work on tax policy in then-leader of the opposition John Howard’s office in the 1980s, Jordan became an advisor to governments on issues ranging from implementation of the GST to becoming chair of the Business Working Tax Group and later chair of the Board of Taxation. He had also become chair of KPMG in NSW.

Approached about the commissioner’s job by the then-Treasury secretary Martin Parkinson, Jordan was appointed on January 1, 2013 by then-Labor Treasurer Wayne Swan, whose chief of staff at the time was one Jim Chalmers. ‘‘I had a bit of impostor syndrome,’’ Jordan says with a laugh.

‘‘I thought, ‘why me? I couldn’t do that. It’s ridiculous’. And then I thought, ‘Well, why not me? I would like to do that and actually make change’.

‘‘That’s because it was obvious to me that the reputation of the Tax Office had shifted a bit from being the top of its class to being more rigid. I was incredibly impressed with the way they did that huge implementation of the GST and all of that, but they seemed to have drifted off a bit after 2000.’’

Jordan says his clear mandate was to try to make the ATO more connected to the community and more aware of community needs and expectations.

‘‘I was firmly of the view that you needed to make staff as satisfied as they can be at work to be able to deliver a satisfactory service for people. If you are all bound up in bureaucracy and process, that’s what you will do to clients whether external or internal.’’

Yet, he is noticeably frustrated that strict secrecy laws governing the ATO have made it harder for the agency to simultaneously demonstrate its commitment to greater transparency and accountability. The unravelling at PwC has sharpened all those contradictions.

The savage criticism has included why the Tax Office did not reveal its suspicions about former PwC partner Peter Collins, leaking sensitive material – including by Jordan informing the Secretary of the Treasury.

‘‘It’s a difficult and fine line to walk but I believe there are very sound reasons to change the secrecy provisions to provide better opportunity for the Tax Office to share information, particularly with other government departments,’’ Jordan says. ‘‘It’s a bit odd that I can’t tell the Secretary of the Treasury certain things.

‘‘There is a review being done by Attorney General’s of all the secrecy provisions, but I would like some specific changes made to our secrecy provisions to enable us to be more effective and efficient.’’

That, according to the tax commissioner, should also include greater ability for the ATO to undertake criminal investigations itself rather than relying on the Australian Federal Police, and to broaden its scope from merely making tax assessments to allow closer examination of potential fraud.

‘‘This is the whole problem that we had with the PwC Peter Collins issue – that we didn’t have the power to ask PwC for certain information because it wasn’t to do with the making of an assessment to tax,’’ Jordan says.

He believes the outcry will lead to an overdue focus on the regulatory governance of partnerships and whether they should become subject to ASIC’s normal corporate governance requirements. ‘‘I personally think that would be well worth looking at.’’

Yet, the ATO’s adherence to the tax secrecy laws also led to a turf war with the Tax Practitioners Board after the ATO had referred Collins to it.

The Financial Review’s story on the board’s decision to deregister Collins as a tax agent triggered the detonation of PwC’s reputation. The ripple effects are still spreading through the big four consultancies and their previously highly lucrative government services businesses.

The TPB’s subsequent decision to also access the ATO’s confidential files of its agreements with 24 international companies without prior notice or permission created considerable friction between the two agencies, coming to a head at a meeting in September 2021, also revealed by the Financial Review.

‘‘They came into our systems without telling us and took a number of highly confidential settlements,’’ Jordan says now.

‘‘This thing about shouting and all, that didn’t happen. But I was very direct and very clear that this was not the way to have a good relationship.’’

Some of these files, he says, also had nothing to do with the PwC matter.

‘‘We simply asked, why did they need those documents? We never heard back and now we are labelled as obstructionist.’’

That’s unlikely to accord with the TPB’s version of events

But what can’t be disputed is that Jordan, from the time he started at the ATO, has been far more effective in his dogged pursuit of multinational companies, including the new generation of tech giants such as Apple, Google and Microsoft. He argued they were using all sorts of accounting techniques to unfairly reduce the amount of tax paid locally, despite the revenue made from selling their products here.

This notion of profit shifting or transfer pricing was hardly new or limited to Australia. Many national governments have found it hard to establish appropriately taxable sources of revenue due to slippery notions of intellectual property rights deliberately allocated to low-tax jurisdictions.

Years of OECD efforts to establish global rules on ‘‘base erosion and profit shifting’’ are still dogged by disagreements, despite Australia’s leading role in encouraging greater international co-operation between national tax authorities.

Ironically, Jordan’s strong support for Australia’s own version of multinational anti-avoidance legislation under the Coalition government led indirectly to the inferno at PwC.

Then PwC partner Collins used his confidential consultations on the legislation with Treasury to brief dozens of his partners ahead of it coming into effect on January 1, 2016. PwC then used this material with potential international clients to immediately promote tax strategies to bypass the legislation – inadvertently alerting the ATO to investigate how the countermeasures could have been adopted so quickly.

Nor were the biggest and more traditional resources companies immune from the ATO’s targeting as it separately successfully challenged companies such as BHP and Rio over their use of assigning big profits to marketing hubs in low-taxing Singapore.

Similarly, the ATO won a hard-fought, crucial court case in 2017 over Chevron providing an artificially high interest-rate loan to its Australian arm which reduced stated profits and thus tax liabilities.

Jordan describes this as one of carefully structured ‘‘debt dumping’’ schemes – advised by none other than PwC – and it took the ATO $10 million and several years to win the fight.

According to Jordan, the court judgment meant oil and gas companies forfeited an estimated $40 billion in interest deductions that would have been carried forward – resulting in $12 billion of additional tax being paid in Australia. He says he is now ‘‘very satisfied’’ with the tax arrangements for multinationals.

‘‘We (the ATO) used to be intimidated by firms coming in and dropping a big report on the table and saying it had been done by world experts. Who are you to question the results,’’ he says.

‘‘I said, ‘Don’t go through each page and tick it as being correct and therefore the result is correct. Stand back and look at what has been done and if it doesn’t make sense economically, you should not just accept it’s correct technically. Really challenge it’.

‘‘We might have disagreements still. But we know what they are doing and they know if and when they will have a disagreement with us.’’

That includes lengthy court battles with Coca-Cola and PepsiCo over the ATO’s application of a ‘‘diverted profits tax’’ with Pepsi currently appealing a federal court judgment in the ATO’s favour last December.

The result, according to Jordan, is that there’s ‘‘not a lot of tax left’’ in what the ATO used to think of as a large corporate tax gap.

But Jordan’s optimistic view that most people now think large companies are paying their share of tax is likely to be tested given the ATO’s focus on extending its focus on the ‘‘tax gap’’ to more small businesses and individuals.

The ATO’s leniency towards many small businesses during the COVID-19 era is now gone. Over the five years to 2023, the ATO’s uncollected debt almost doubled to over $50 billion.

‘‘The small business area debt has grown very significantly,’’ Jordan says. ‘‘A number of small businesses have been living off money that was never theirs . . . if, for whatever reason, the business is not viable, they need to understand that.’’

As for Australia’s extremely heavy reliance on income tax for revenue, Jordan notes that’s ‘‘policy with a capital P’’ which prevents him commenting. But he points out that most countries have shifted to taxes on property and consumption. ‘‘We seem to have this problem that you can’t raise an issue without it being shut down before it’s actually talked about.’’

He also cites the fact that Australians are big users of workplace expense deductions, making individual tax returns far more complicated.

New Zealand, he says banned workplace expense deductions while also dropping the top marginal tax rate to 30 per cent. Due to that simplicity, most New Zealanders get their returns simply pushed to them due to forms being ‘‘pre-filled’’ with the necessary information.

‘‘We will find it hard to get to that situation because of work-related expenses,’’ he says.

Jordan’s last public outing as tax commissioner before he exits on February 29 will be at the National Press Club next week. He will wait until midyear to decide what comes next.

‘‘I have no particular plans,’’ he says. For about the first time in his life. AFR

{kind=link}

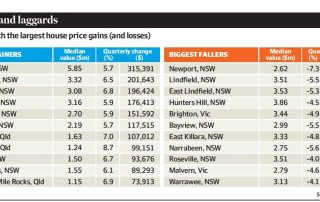

Suburbs where house prices fell $200k in three months

House prices in some of the country’s most desirable suburbs have slumped by as much as $207,000 in just three months, dragged down by the ongoing weakness in the upper end of the housing market, data from CoreLogic shows.

By contrast, house values in some of the middle-priced suburbs and those with low stock levels jumped by up to $315,000 over the same period.

CoreLogic research director Tim Lawless said the upper end of the housing markets in Sydney and Melbourne continued to weaken, while the middle to lower end stayed relatively resilient.

Over the past three months to January, the top 25 per cent of Sydney’s housing market by value has dropped by 0.2 per cent, extending its 0.1 per cent fall in the previous three months.

In comparison, the middle segment of the market posted a gain of 0.6 per cent, while the lower quartile rose by 0.2 per cent.

Similarly, in Melbourne, the upper end led the decline, with values falling by 0.5 per cent, while the lower end dipped by 0.4 per cent.

Mr Lawless said the more affordable end of the housing market could see faster growth once interest rates started falling.

‘‘Lower interest rates will have a broad-based benefit as it lifts borrowing capacity for everybody, so in that sense, it floats the entire housing market rather than just one individual area,’’ he said.

‘‘But I think we could see a more pronounced impact in some of those markets where households are more sensitive to interest rates, such as the middle to lower end of the marketplace.

‘‘We could see a real pickup in first home buyers taking advantage of the lower rates alongside a lot of the concessions or incentives that exist in the marketplace as well. I think a lot of people will also be trying to take advantage of the Sydney and Melbourne markets where prices have dropped below their recent record highs.’’

Sydney’s northern suburbs and upper north posted some of the largest declines in house values in the past three months.

Houses in Newport on the northern beaches tumbled by 7.3 per cent in value, slashing $207,474 from the median to $2.62 million. Narrabeen, Bayview and Bilgola Plateau also lost more than 5.3 per cent, or around $154,000. Lindfield, East Lindfield and East Killara on the upper north shore also recorded sharp quarterly declines in house values, falling by 5.5 per cent, 5.3 per cent and 4.8 per cent respectively. Their medians are now lower by around $176,000 on average.

In Melbourne, house prices across Brighton, Caulfield North, Malvern and Caulfield fell by at least 4 per cent, shedding up to $178,000 in median house value.

House prices in Brisbane’s inner-city suburbs Teneriffe, Alderley and Wooloowin fell by 1.8 per cent on average or up to a $61,900 drop in their median values.

By contrast, house values in some middle-priced and tightly held suburbs bucked the slowdown and posted healthy gains in the past three months.

In Sydney, Haberfield in the inner west clocked the largest increase of 6.8 per cent or a nearly $200,000 lift in the median to $3.08 million. Neutral Bay and Mosman on the lower north shore also notched up sharp quarterly increases of 6.5 per cent and 5.7 per cent respectively, adding $201,643 and $315,391, to their median house price respectively.

Sydney-based real estate agent Thomas McGlynn of BresicWhitney said buyers had become price conscious in the past three months.

‘‘We saw a real flight to value, that’s why we’re seeing good growth in some pockets of the inner west, where houses are still priced lower than their premium counterparts,’’ he said.

‘‘Some expensive suburbs such as Mosman simply have no stock, so buyers have to compete fiercely when a property comes on the market, pushing prices even higher.’’

In the regions, the towns where house prices plummeted the most in the past year have bounced back strongly in the past three months, according to CoreLogic. Richmond-Tweed towns Lismore Heights, North Lismore and Lismore logged at least 8 per cent house price gains.

House prices in Mortlake in regional Victoria and Leyburn in regional Queensland increased by 6.2 per cent and 8.1 per cent respectively.

‘‘The lift in house prices in those regions could be a sign that more buyers are taking advantage of the fact some of these areas have become a bit more affordable after their recent price declines,’’ Mr Lawless said.