Top property picks for 2022

AFR Article 19 December 2021.

Housing market With many suburbs already hitting record highs, investors need to conduct thorough research to avoid paying above market value. Nila Sweeney highlights 11 areas with potential.

The housing market is predicted to slow significantly in the year ahead and even contract once interest rates start rising later next year, but there are plenty of opportunities for investors looking to cash in on the next wave of growth, experts say.

The rapid rise in home prices also forced many aspiring homebuyers back into renting, fuelling a surge in demand for rental accommodation.

During October, the vacancy rate fell to a decade low of 1.6 per cent nationwide, SQM Research data shows.

‘‘I think it’s a good time to invest because money is still cheap and people have a lot of disposable income,’’ says Victor Kumar, a buyer’s agent specialising in investment property at Right Property Group.

‘‘The greatest catalyst for growth is yet to come – the reopening of the border and restarting immigration. So if you’ve bought the right property in the right area, you’d do well. You just need to be careful as to what and where you’re buying.’’

With many areas already hitting record highs, investors need to conduct thorough research to avoid paying above market value, says Peter Koulizos, program director at the University of Adelaide’s School of Architecture and Built Environment.

‘‘The main risk is paying too much for a property, with so many people paying ridiculously high prices for property at the moment,’’ he says. ‘‘Once this boom is over, property prices will flatten, and in some locations may dip slightly. You don’t want to be in negative territory when the market slows.’’

It is also important to focus on the long term, not on small price movements as they tend to be immaterial over a decade, says Doron Peleg, co-founder of buyer’s agency BuyersBuyers. ‘‘Try instead to think about where prices will be 10 years from now.’’

So which areas offer potential for strong capital growth and rental returns? Here are the experts’ top picks.

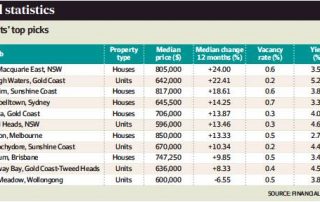

Wynnum, Brisbane: Pete Wargent, cofounder of BuyersBuyers, picks Wynnum for its good transport links and city access, proximity to water and desirability for buyers and renters alike. ‘‘Rental vacancy rates are very tight in Wynnum, at just 0.5 per cent, and we expect rents to rise strongly in 2022 and beyond,’’ he says.

Carrara, Gold Coast: ‘‘The rental market on the Gold Coast is very tight due to strong internal migration. With rents rising quickly, the market is attractive for landlords,’’ says Wargent.

‘‘Rental vacancy rates are extremely tight in Carrara, at just 0.3 per cent – as close to zero as you’ll likely ever see – and we expect rents to rise strongly in 2022 and beyond.’’

Buderim, Sunshine Coast: ‘‘Buderim has a fine, elevated position yet is still relatively close to the beaches,’’ says Wargent. ‘‘The centre of Buderim has a strong community vibe and attractive small-town feel.’’

Rental vacancy rates are tight, at just 0.6 per cent, and rents are set to rise strongly in the near to medium term.

Croydon, Melbourne: ‘‘The suburb has strong connectivity and transport for the city with its bus and rail links, and has homes on attractively spacious blocks of land, which will appeal to families,’’ says Wargent.

Rental vacancy rates are tight, at just 0.5 per cent.

Campbelltown, Sydney: Affordability will begin to bite for houses in Sydney’s top-performing suburbs next year, but there are still suburbs and pockets where prices have not yet soared out of reach, says Wargent.

‘‘Campbelltown to the south-west of Sydney covers a large area, and buyers need to choose their asset carefully, but there are still potentially attractive entry points for buyers looking for detached-house investments,’’ he adds.

Burleigh Waters, Gold Coast: Units are not cheap, with the median at the end of November touching $650,000. But demand is high relative to supply, says Jeremy Sheppard, research director at Select Residential Property. ‘‘Units spend about a month listed for sale before being snapped up. That’s about three times faster than the long-term, national average advertising period,’’ he says. ‘‘Median rents have climbed an impressive 25 per cent in the last 12 months taking the typical yield up over 5 per cent. A tight vacancy rate of 0.2 per cent should lead to even further rent rises,’’ he says.

Fairy Meadow, Wollongong: More than 40 per cent of units listed for sale are to be sold by auction, indicating strong demand from buyers.

‘‘There is a strong probability this suburb is about to enter its next growth phase,’’ says Sheppard. ‘‘Searches made online for property in Fairy Meadow are around 1300 per property listed for sale. This is a reflection of strong demand relative to supply.’’

Tweed Heads, Gold Coast: The vacancy rate for units in Tweed Heads at the end of November was 0.3 per cent. Rents have increased by 12 per cent over the past year, leading to a healthy yield of 4.6 per cent. Growth in neighbouring suburbs over the last year has been a lot higher than Tweed Heads. That growth should flow over into Tweed Heads, says Sheppard.

Runaway Bay, Gold Coast: The median unit price at the end of last month was $636,000. And while selling times are a bit sluggish, a 100 per cent auction clearance rate suggests there’s heat in this market from buyers, says Sheppard. ‘‘The vacancy rate is just 0.4 per cent leading to some good growth in rents and a yield of 4.5 per cent,’’ he adds.

Maroochydore, Sunshine Coast: Units are going for $670,000 and achieving a 4.4 per cent yield, says Sheppard. ‘‘Yields had climbed with rents rising 19 per cent in the last 12 months, but they could go even higher in the coming year with a vacancy rate of only 0.2 per cent,’’ he says. ‘‘Demand is ahead of supply, indicated by one in two properties listed for sale being sold via auction.’’

Lake Macquarie East, NSW: The three suburbs of interest are Tingira Heights, Cardiff Heights and Macquarie Hills, says Kent Lardner, research director at Suburb Trends.

‘‘There’s a lake on one side and beaches on the other, with plenty of national parks and hills to capture views,’’ he says.

‘‘It’s an easy commute to Sydney once or twice a week and buyers are flowing up from the Central Coast and down from Newcastle.

Weekly rents for houses have increased by $50 in the last 12 months with vacancy rates for the area currently 0.66 per cent.SI

{kind=link}