How COVID-19 changed the market

The COVID-19 housing boom may have peaked in most parts of Australia but analyst CoreLogic has identified six ‘‘remarkable’’ shifts caused by the pandemic over the past two years that will have a long-term effect on national property markets.

Record house prices and buyer debt lead the pack. Close behind are rental increases and yield falls, a spike in first-home buyer numbers, the shift to the country and a widening chasm between house and unit pricing.

‘‘The global pandemic has catalysed remarkable shifts in the Australian housing market,’’ CoreLogic says in a new report, Two years on: Six ways COVID-19 has shaped the housing market.

‘‘From the temporary shutdown of cities, to an unprecedented monetary policy strategy, the COVID-19 period has had distinct impacts on the composition of buyers and the dynamics of the housing market.’’

The most obvious impact is on housing prices. According to CoreLogic’s Home Value Index, home values across Australia leaped 25 per cent to record highs in the two years to the end of February. The median national dwelling value increased $174,000 to $728,000 over the same period.

First home buyers, fuelled by grants such as the federal government’s HomeBuilder payments, fired up the market in 2021, mirroring what happened a decade before when the First Homeowner grant was temporarily boosted in 2009-10.

But that turned out to be a sugar hit and when the government money dried up and house prices increased, first-home buyer demand returned to its long-term average of 24 per cent of all owner-occupiers.

Through this period rents rose 12 per cent, once again to record highs, the fastest growth since 2008.

Conversely, gross yields for investors fell to a record low of 3.21 per cent as purchase prices increased at a faster rate. The median national rent is now $470 a week.

‘‘As housing growth has started to slow, this record low gross rent yield figure appears to have begun stabilising,’’ CoreLogic said.

Housing debt surged, obliterating previous benchmarks, as buyers borrowed more to get into a fast-moving market.

The ratio of housing debt to household income reached 140.5 per cent in the second half of 2021. Home loan volumes are still exceptionally high, with new loan commitments totalling $33.7 billion in January.

CoreLogic said rising debt levels ‘‘creates a vulnerability’’ in the Australian economy, but high asset values and low interest rates reduced the risks, it said.

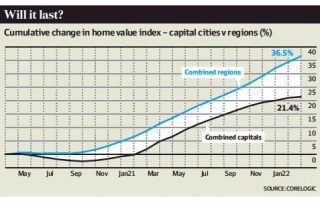

People want more space than ever, driving trends five and six: the divergence of house and apartment prices and much higher levels of migration from cities to the regions.

When combined with a shortage of stock, this caused regional housing prices to grow at almost twice the speed of city properties – 36.5 per cent compared with 21.4 per cent.

However, growth in most markets is now moderating, the report says.