What It Means For Your Money

There are numerous opportunities for astute investors and consumers to take advantage of. Aleks Vickovich and our expert writers break it down.

As expected, the Morrison government’s pre-election budget had plenty of sweeteners. The 2022-23 budget documents revealed total expenditure of $628.5 billion, of which social security and welfare ($221.7 billion) made up the lion’s share, alongside funding for health ($105.8 billion), education ($44.8 billion), defence ($38.3 billion) and transport and communications ($18.9 billion).

Included was a one-off, $8.6 billion package of short-term handouts described by The Australian Financial Review as a ‘‘shameless voter bribe’’.

Whether the cash splash is effective remains to be seen, with voters to go to the polls in May. But the budget’s short- and long-term measures contain a range of opportunities that astute investors and consumers may seek to take advantage of.

Here’s what you need to know.

Women

Australian women remain on track to earn $2 million less than their male counterparts due to what economists and critics deem a lacklustre, pre-election federal budget.

While it included $9 million in funding to support emerging female entrepreneurs and $58 million in funding for endometriosis, experts warn the measures do not go far enough to promote women’s earnings capacity and – in the case of the paid parental leave changes – may even backfire.

The government’s paid parental leave scheme will now be 20 weeks shared at the couple’s discretion at the minimum wage. Previously, primary carers – who tended to be mothers – were eligible for 18 weeks, while partners were eligible for two weeks. The income test will be changed to a household limit of $350,000 each year rather than the individual test.

‘‘It’s done under the guise of flexibility and allowing more leave sharing between partners,’’ says Grattan Institute CEO Danielle Wood. ‘‘That’s great in the small percentage of households that want to do that, but my theory is it will actually lead to more gendered norms around who cares [for children] in the early years.’’

That policy, coupled with no movement on childcare, confirms Grattan modelling that finds the average mother will earn $2 million less over her lifetime compared to the average father, says Wood.

‘‘[The budget] was a missed opportunity to address some of the disincentives to women’s workforce participation, particularly the higher cost of childcare,’’ she adds.

Industry groups also characterised the budget as lacking for women.

Tax Institute analysis of childcare costs and subsidies found the secondary earner, who is often the mother, faces a steep disincentive to return to full-time paid work.

‘‘If they’re back to a full-time schedule, the secondary earner is only gaining $6 extra for the tenth day of work in a fortnight. By the time they’ve commuted to work and bought a morning coffee, they’re paying to go to work that day,’’ says Tax Institute tax policy and advocacy general manager Scott Treatt.

‘‘The secondary earner in a family can be taxed at an effective rate, including net childcare costs, of more than double the top personal marginal tax rate. This makes returning to work financially impossible for many parents who might otherwise like to.’’

LUCY DEAN

Retirees

In a measure foreshadowed by the Financial Review in March, the government committed to extending its changes to the superannuation minimum drawdown requirement for another year. ‘‘The government has extended the 50 per cent reduction of the superannuation minimum drawdown requirement for account-based pensions and similar products for a further year to June 30, 2023,’’ the budget documents said.

‘‘The minimum drawdown requirements determine the minimum amount of a pension that a retiree has to draw from their superannuation in order to qualify for tax concessions.’’

Drawdown rates range from 4 per cent to 14 per cent, depending on age. The extension of the halved rate would drop the rate from 7 per cent to 3.5 per cent for someone aged between 80 and 84.

While the budget billed this measure as ‘‘supporting retirees’’, experts say it would really only benefit retirees who have already accumulated substantial wealth outside super.

Peter Burgess, deputy chief executive of the SMSF Association, says the extension allows individuals who have access to outside funds to withdraw less than they would ordinarily have to under the normal policy conditions.

‘‘This means they can retain more in their super pension account – which is tax-free – for longer,’’ he says.

The tax benefits of keeping more money in a super environment are clear, says Lisa Papachristoforos, a partner at accounting firm Hughes O’Dea Corredig.

Wealth held in a super fund in pension mode incurs no tax on income and capital gains, she points out – as opposed to income held in an individual’s name, which is taxed at marginal rates.

But tax advantages are not the only potential benefit. The extension of the minimum drawdown also provides ‘‘continued flexibility’’ on how much retirees need to withdraw to fund standard of living, Papachristoforos adds.

Aside from tax efficiencies, leaving more money in super means more can be invested, generating further returns.

Plus, while the policy may be aimed at retirees, all super fund members may profit from the extension regardless of their age or distance from retirement.

‘‘Super funds are potentially faced with an additional year of lower minimum pension withdrawals paid to their members, allowing them to utilise that forgone withdrawal at a pooled level for investment purposes,’’ Papachristoforos says.

‘‘As such, extending the minimum drawdown rule could positively affect all superannuants, not just those drawing an income stream from their account, and the investment managers of super money will have more funds to invest.’’

Certified financial planner Josh Dalton, of Dalton Financial Planners, agrees there are potential tax minimisation benefits from the extended minimum drawdown policy, as well as the prospect of opening up more money to be invested in markets.

But he warns the measure is not suitable for all retirees. ‘‘Retirees need to estimate their annual expenditure and get a good grasp on how much income they can live on comfortably,’’ he suggests.

‘‘They can then decide to reduce their pension payments in line with their budget estimate and conserve more of their account-based pension capital if it suits.’’

ALEKS VICKOVICH

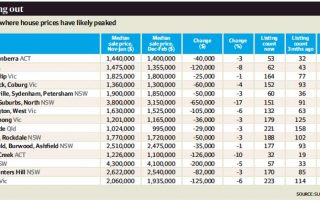

Home buyers

Borrowers planning to apply for the expanded Home Guarantee Scheme should start preparing their applications soon because competition is expected to be fierce, say lenders.

First home-loan applications surged when previous allocations were announced to allow first home buyers and single parents to get into the property market with a deposit of between 2 per cent and 5 per cent without needing to pay for expensive lenders mortgage insurance.

Applicants need to choose a loan from a lender on the scheme’s list that offers the rates, terms and conditions best suited to their needs. It has to be a principal and interest loan. Investors are not eligible.

Prospective borrowers should gain pre-approval for their loan from the lender, which will involve providing identification, age, proof of income, a prior property ownership test, proof of deposit and intention to be an owner-occupier.

Applicants also need to ensure their loan application is within the price caps set for each city. For example, it is capped at $800,000 for Sydney’s central business district and $500,000 for Ballarat in regional Victoria.

The First Home Guarantee, which supports eligible first home buyers to build or purchase a new or existing home with a 5 per cent deposit, has been increased from 10,000 offers to 35,000 a year from July 1. It is capped at $125,000 annual income for individuals and $200,000 for a couple.

There are also 5000 places for the Family Home Guarantee, which enables eligible single parents with dependents to enter or re-enter the housing market with a deposit from 2 per cent.

Mortgage broker Elodie Blamey says single mothers and fathers can earn up to $125,000 – excluding childcare support – to be eligible. ‘‘Unlike the Home Guarantee Scheme, it is not being used nearly enough,’’ she says. Many single parents might not be aware of the scheme and its conditions, or consider themselves eligible.

Merinda Brooks, a single parent with a three-year-old son, says: ‘‘It has absolutely changed my life.’’

The speech pathologist says it would have been challenging to save a 10 per cent deposit. ‘‘I was working really hard but unsure about how I could have otherwise got a deposit together,’’ she adds.

There are also another 10,000 places a year under the Regional Home Guarantee scheme for anyone who has not owned a property for five years, on the condition they purchase a newly built home or build.

Lenders are awaiting additional details from the government before advising potential borrowers.

DUNCAN HUGHES

Patients

Government changes to the Pharmaceutical Benefits Scheme safety net thresholds, making medicines more affordable, is good news for many self-funded retirees, according to a leading super specialist.

Lower safety net thresholds for the PBS mean potential savings for retirees, and may create an opportunity for others who have ‘‘grandfathered’’ account-based super pensions.

From July 1, the PBS safety net thresholds will be reduced from $326.40 to $244.80 for concession patients, and from $1542.10 to $1457.10 for general patients, which means fewer scripts before the safety net is reached.

Patients will also reach the safety net sooner with 12 fewer scripts for concession patients and two fewer scripts for general patients.

‘‘This is good news for self-funded retirees who do not hold a Commonwealth Seniors Health Card,’’ says Colin Lewis, head of strategic advice for Fitzpatricks Private Wealth.

‘‘There may also be the opportunity for advisers to consider clients who have an underperforming ‘grandfathered’ account-based pension but feel trapped for fear of losing the card if they move.’’

Many CSHC holders have account-based pensions that are ‘‘grandfathered’’ after the income test rule change on January 1, 2015. Account-based pensions started after that date are deemed under the card’s income test, whereas nothing counted with existing pensions. For this reason, many are reluctant to switch pensions or super funds for fear of losing their CSHC.

‘‘It is a matter of doing the numbers.’’ says Lewis. ‘‘Deemed income from a new pension may not push a cardholder over the CSHC income threshold but, where it does, the cost of losing the card is now reduced with a lower safety net, and the potential return from a new pension may well exceed this cost.’’

The same concern may contribute to some self-funded retirees maintaining self-managed super funds rather than switching to a possibly better-performing and cheaper retail or industry fund.

DUNCAN HUGHES

Small business owners

Improving workforce skills, incentives for employing apprentices and increasing investment in technology and digitisation are among the opportunities. Small and medium businesses with a turnover of up to $50 million are getting an additional 20 per cent deduction for the cost of external training provided to employees.

That means a business will be able to deduct $120 for every $100 spent on a course.

As an example, a business needs to train 10 employees in administrative skills to manage jobs. The company enrols them at a cost of $430 per employee. In addition to the $4300 deduction, the company can claim an additional $860 deduction, being 20 per cent of the expense.

There is also $2.8 billion over five years to increase apprenticeships, including $5000 payments to apprentices over the first two years of their apprenticeships, and $15,000 to qualifying employers paid as 10 per cent for first- and second-year apprentices and 5 per cent for third-year workers.

For example, a business employing an apprentice for $40,000 a year will receive $1250 every six months for two years to help with the cost of training. The company can apply for payments of $4000 in the first and second years, and $2000 in the third year.

The calculations were provided by financial adviser Cameron Harrison.

Businesses are also eligible for another 20 per cent deduction for expenses on digital upgrades, such as cyber security systems or subscriptions to cloud-based services, up to $100,000. Installation has to be completed by June 30, 2023 to be eligible.

‘‘This is a no-brainer,’’ says Greg Travers, a director of William Buck. ‘‘Businesses know they need to digitise, and now the government is giving them an incentive to do it. The benefit is not huge . . . but it helps.’’

Digitisation means more pre-filling, data-matching and data-sharing for the Australian Taxation Office.

‘‘The measures are designed to reduce compliance costs for businesses, but also make it easier for the ATO and other revenue authorities to data-match and share information,’’ Travers says. These measures include using real-time data to calculate PAYG tax instalments.

Sam Pratt, chief executive of Render Networks, which develops broadband connectivity, says while it was a good budget for infrastructure, there needs to be more support for the digital economy to keep it competitive with the US and Europe.

Changes to the taxation of employee share schemes will help smaller companies, particularly technology start-ups, attract and retain skilled workers. Limits on the value of shares an employer can issue to employees has been increased from $5000 to $30,000, which puts it in line with international standards.

DUNCAN HUGHES

Aged care residents

With medication management long regarded as the bane of residential aged care, funding to link care facilities with community pharmacists and onsite pharmacists should bring some comfort to residents and nurses.

The delivery of wrong and/or excessive medication has long been an issue waiting to be addressed.

However, at the heart of this and other positive reforms flagged for the aged care sector in the federal budget lies a major problem – recruiting and retaining qualified staff.

Notably absent from the spendathon was any mention of the wage increase for existing or future aged care workers that is so desperately needed to deliver the existing services, let alone promised ones.

Pharmacists are as desperate for the implementation of a workforce plan as the aged care sector, putting a huge question mark over the success of a potentially good idea before it is even rolled out.

The ongoing release of 80,000 home care packages in 2021-2023 – taking the total to about 275,600 people by June next year – is welcome confirmation of intentions to assist older Australians to remain living independently at home.

But the delivery of the packages and other at-home support is also dependent on attracting a suitably skilled workforce to meet the demand.

It is the same for the 8500 new respite services also announced previously as part of an $18.8 billion, five-year reform program following the Royal Commission into Aged Care Quality and Safety.

On that front, the $48.5 million for 15,000 additional aged care training places for new and existing personal care workers, to a total of 48,800 places, is a positive move.

More money for more training is always welcome, says Sean Rooney, chief executive of Leading Age Services Australia and representative of the Australian Aged Care Collaboration. But he says the budget failed to address the key fundamental deficiencies identified in the royal commission – wages and the viability of aged care homes.

Sticking with the commitment to reform the residential aged funding model through the introduction of the Australian National Aged Care Classification Transition Fund, the budget included an additional $34.60 per bed per day.

The proposed residential aged care funding model, scheduled to begin on October 1, is designed to align residential aged care funding to the care needs of each resident.

The starting price is $216.80 a day per resident for standard care – with more for dementia-related care – compared to about $180 a day per resident under the old funding model.

Council on the Ageing chief executive Ian Yates will be looking to see that the additional money is spent on increasing the number of care minutes with residents as intended by the royal commission, which recommended care homes have a target of 200 minutes per resident per day.

Exactly how that will be measured is yet to be worked out. But Yates wants the government to commit to publishing how many minutes of care each residential facility is being funded to deliver, compared to the number of minutes actually delivered, as part of its new star rating system.

With an election on the way, there is still hope for further announcements that will directly benefit older Australians and those who deliver the care they deserve.

Unlike the government, the opposition has centred its budget promises on fixing the aged care workforce with a $2.5 billion pledge for measures, including a wage rise.

BINA BROWN

Young Australians

Successive budgets chasing the ‘‘grey vote’’ have allowed structural flaws in Australia’s economy to form, with younger generations and economists now calling for bold conversations to help strike out the unwieldy debt bill.

The budget features a projected $78 billion deficit for 2022-23. The deficit is expected to linger for the next 10 years, with gross debt peaking in 2025.

While a deficit isn’t necessarily a problem if the debt brings sustained productivity or lifestyle improvements, Australia’s ability to wind back high levels of spending will be the key issue for younger generations, says the Grattan Institute’s Wood. ‘‘We shouldn’t be so fixated on the deficit per se, especially coming out of COVID-19; it partly reflects that we did need to spend a lot to respond, and that it was appropriate to do so,’’ she says.

‘‘But we should think about the structural budget deficit over time, and that does look a bit concerning.’’

Wood says Australia’s spending appears to be fixed at a higher level after COVID-19, with more money flowing through to defence, aged care and the National Disability Insurance Scheme.

‘‘We haven’t really talked about how we’re going to pay for that over time,’’ she says. ‘‘The risk is if we don’t do anything about that and debt continues to creep up as a share of the economy – that’s the concern that young people, quite rightly, might have.

‘‘It’s that longer-term picture and the lack of clarity around how we’re going to square those numbers.’’

The co-founder of intergenerational fairness advocacy group Think Forward, Sonia Arakkal, agrees government debt is a complex issue, but is concerned that the budget puts older generations’ needs before younger generations’ current and future needs.

‘‘Young people have a sophisticated understanding of the economy – we’re a very highly educated generation . . . we want policymakers to take into account our interests,’’ she says.

‘‘So, if they are accruing debt in our name, it should be debt that is invested in climate change or infrastructure – not pork-barrelling in particular marginal seats or particular states.’’

Faced with baked-in higher spending, an ageing population and a need to decarbonise, Arakkal – who is leading calls for a parliamentary inquiry into intergenerational fairness – is calling for Australia’s political class to engage in more difficult conversations about equality.

‘‘We have a system that is overly reliant on income taxes and doesn’t treat asset taxes in the same way, and we shouldn’t be punishing people for working. We should be looking at taxes that are inefficient, like capital gains tax, or how we tax superannuation,’’ she says.

‘‘We need to be having those conversations to set the younger generation up for success.“

There are two options for tackling the deficit, says Wood.

The first is to find ways to make the economy grow faster, as a faster-growing economy will essentially ‘‘fritter away’’ the debt burden.

‘‘Looking at policies which actually promote productivity and growth is important, so that could be tax reform, reforming cities, and how we do planning and zoning regulation?’’ she says.

Supporting more women to return to the paid workforce after having children is also a key way to uncap economic potential, Wood says, expressing disappointment at the budget’s muted changes in that area.

‘‘Over time, I think taxes will have to rise, even if we do tick some boxes on the growth front,’’ she says.

‘‘It’s inevitable that as government has increased as a share of the economy, that there will have to be an increase in taxes to pay for that. That has to be done carefully. What we shouldn’t do is just rely on income tax to do all the heavy lifting, which is what we’ve done historically.’’

LUCY DEAN

Households

Those earning up to $126,000 will be eligible for an additional one-off $420 that will be paid when their 2022 tax return is lodged. There’s also a one-off cost of living payment of $250 to eligible income support recipients and certain concession cardholders. Fuel excise (a federal tax imposed on each litre of petrol) will be halved, intended to reduce the cost of fuel by 22¢ a litre. In addition, costs of taking a COVID-19 test to attend work are tax deductible from July 1.SI

DUNCAN HUGHES