AUSTRALIA’S GREAT DEBT GAMBLE

AFR Review 3-4 July 2021. Page13

Intergenerational report Policymakers are betting on low rates and solid growth, writes Ronald Mizen.

Tony Abbott and Joe Hockey’s infamous 2014 budget became so toxic it ultimately destroyed its makers; the task facing Prime Minister Scott Morrison and Treasurer Josh Frydenberg is orders of magnitude bigger.

Abbott and Hockey won an election on a platform of fixing Labor’s ‘‘debt and deficit disaster’’, but in the end, the job of selling fiscal repair was overwhelming for the former prime minister and his treasurer.

Not even the highly politicised release of the 2015 Intergenerational Report, which outlined an economic renaissance over the four decades hence if people embraced the duo’s policies, helped.

The fall from grace was swift. Throw forward a little more than half a decade, and Morrison and Frydenberg face a more complex set of challenges.

In financial year 2015, net debt was about 14 per cent of economic output, and the deficit was expected to be $30 billion, or about 1.8 per cent of GDP (which included an additional $8 billion spent by the Coalition).

Today, net debt is forecast to peak at 40.9 per cent of GDP and the deficit is expected to hover between 2.4 per cent and 5 per cent of GDP for some years.

Labor points to the global financial crisis and its more than $70 billion in economic stimulus between 2008 and 2009 as the root cause of the budget deterioration during its time in government.

The Coalition opposed much of this spending, which, as then opposition leader Malcolm Turnbull later said in his biography, made Abbott’s and Hockey’s eventual debt and deficit campaign possible.

In stark contrast, few criticise the almost $300 billion spent in direct economic support to help the nation through, and out of the COVID-19 pandemic – not only was it appropriate, it was low.

‘‘As a share of the economy, net debt is around half of that in the UK and US and less than a third of that in Japan,’’ Frydenberg said on budget night. But that just makes the eventual repair pitch all the more difficult.

Savings of an order last seen in the 2014 budget – or about $40 billion to$50 billion a year – will eventually have to be made to tame the ballooning bottom line, says Deloitte Access Economics partner Chris Richardson. ‘‘That’s a challenge. To be clear, budget repair shouldn’t start soon. And it can – and should – be slow. But it won’t be fun,’’ he says.

On current settings, Australians are in for 40 years of debt and deficit, this week’s release of the 2021 Intergenerational Report shows. The budget comes within a whisker of balance in 2036-37, reaching 0.7 per cent of GDP before falling away again to 2.3 per cent in 2060-61, a consequence of increased spending and the artificial tax-to-GDP cap of 23.9 per cent.

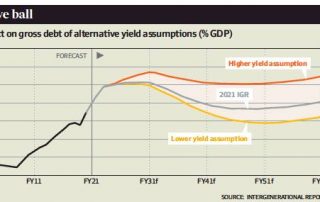

Net debt is expected to hit 34.4 per cent of GDP by financial year 2061, while gross debt – a better determiner of serviceability – reaches 40.8 per cent. And that outcome is on the rosy side – the risk is mostly downside. Dig a little deeper into the document and a very different picture emerges.

Frydenberg argues that, while gross debt has increased significantly since the onset of the pandemic, the cost of servicing that debt is lower in 2021-22 than it was in 2018-19, as a result of historically low interest rates. ‘‘Low yields, together with strong economic growth, means the government can reduce the debt-to-GDP ratio without running a surplus,’’ the 2021-22 budget papers say.

That scenario, of course, assumes low yields and strong economic growth. Sensitivity analysis in the Intergenerational Report shows that if 10-year bond yields converge from their current lows over five years to the long-run rate of 5 per cent, the debt and deficit profile deteriorates dramatically. The deficit increases by 0.6 of a percentage point to about 3 per cent of GDP by 2060-61, which adds about 14 percentage points to gross debt and lifts the outlook to just shy of 55 per cent of GDP.

Indicators generally suggest neither inflation nor bond yields will rise too far in that space of time, says Tony Morriss, Bank of America’s head of Australian economics and rates strategy. ‘‘The two major factors we would need to see would be a sustained rise in global and local inflation and a change in the global structure of interest rates and bond yields, most notably a move away from zero or negative interest rates in Europe and Japan that helped anchor yields since the GFC.’’ he says.

Then there’s the question of ‘‘strong economic growth’’. Productivity accounted for more than 80 per cent of national income growth in the past 30 years, and Frydenberg labelled it ‘‘the most vital ingredient in lifting our long-term living standards and wages’’.

Falling just 0.3 of a percentage point short of the forecast 1.5 per cent average growth rate forecast in the IGR will have significant consequences. Gross national income will be $32,000 per person lower, pushing down government tax receipts and lifting net debt as a portion of the economy to more than 57 per cent by 2060, and gross debt to just shy of 64 per cent.

The overall size of the economy would be $500 billion smaller at about $4.95 trillion (or $127,600 per person) compared with the baseline scenario of $5.46 trillion (or $140,900 per person). Yet actual productivity gains since the 2015 IGR have been barely one-third of the 1.5 per cent rate assumed.

Frydenberg says the ‘‘big bang’’ reforms of the 1980s and 1990s cannot be repeated and future reform will be incremental; but economists are sceptical about whether this will be enough to reverse the trend.

‘‘Even the sensitivity analysis suggestion of 1.2 per cent is incredibly optimistic. If we were able to achieve 1.2 per cent that would be a miracle,’’ says Blueprint Institute chief executive Steven Hamilton.

Big reform, as recent history has shown, is a difficult proposition, especially when the debate has become one where there can be no losers. ‘‘Reforms cost too many votes for governments to even try to champion them,’’ says Richardson.

The Business Council of Australia (BCA) this week pulled up the stumps on waiting for politicians to lead and drive a reform agenda, instead outlining a plan to take its message to the people and build a groundswell of support for reform.

Gross national income per person could be $10,000 better off over the decade if measures are introduced to boost productivity and stop it from ‘‘acting as a handbrake on the economy’’, says BCA chief executive Jennifer Westacott.

That wouldn’t make up for the $11,000 per-person lost over the last decade as a result of what the Productivity Commission calls the worst for productivity growth in more than half a century.

Then there’s the long-term impact on the nation’s population because of the closed international border during the pandemic, and the benefits of making up for this lost ground over the next 40 years.

Australia’s population was forecast to reach almost 40 million by financial year 2055, in the 2015 IGR, but because of COVID-19 and a much-lower-than-forecast fertility rate, it is now likely to reach about 38.8 million five years later.

This comes with a significant cost. But boosting annual net overseas migration from 235,000 a year to 327,000 by 2060-61 would lift real GDP growth from 2.3 per cent to 2.6 per cent by the end of the forecast period, and add $260 billion to the economy.

Closing borders has been politically popular, even while tens of thousands of Australians remain stranded overseas. Some people draw a connection between Australia’s success in lowering the jobless rate and the nation’s tightly sealed international border.

So, while the Intergenerational Report shows the need to not only return migration to previous levels but also boost it to make up for lost ground, the politics of such a proposition could be difficult after the Fortress Australia mindset.

Eventually tough, but necessary, decisions will need to be made on reform, on budget repair and on opening the border.

‘‘What will it take for either side of politics to do something bold?’’ asks Blueprint’s Hamilton. [If] an IGR which shows budget carnage over the next 40-years isn’t enough – what will be enough?’’ P

{kind=link}

{kind=link}